COMMERCE 1AA3 Lecture Notes - Lecture 3: Fiscal Year, Gross Profit, Retained Earnings

18 May 2016

School

Department

Course

Professor

Document Summary

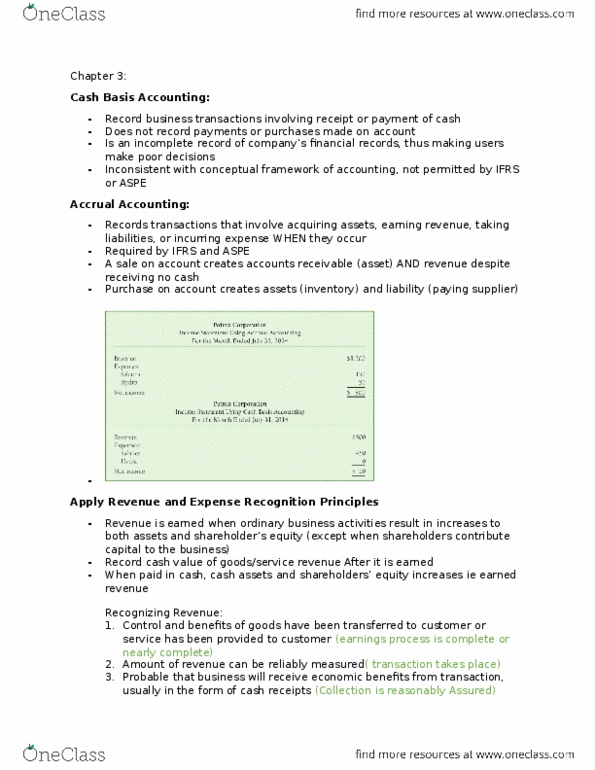

Records the impact of transactions when they occur: revenues when earned/ acquiring an asset, expenses when incurred/ taken a liability. Both cash and non-cash transactions: even if the business receives or pays no cash. Receipt or payment of cash is irrelevant: required by ifrs and aspe. Only records cash transactions: cash receipts (treated as revenues, cash payments (treated as expenses) Ignores other business transactions: results in incomplete financial statements. Not permitted by ifrs or aspe: only used by small businesses. Cash transactions: collecting payments from customers, receiving interest earned, borrowing money, paying expenses, paying off loans. Noncash transactions: sales on account, purchases on account, accrual of expenses not yet paid, depreciation expense, usage of prepaid expenses, earning of revenue when cash was collected in advance. Going out of business: shut down, sell assets, pay liabilities, return leftover cash to owners, only way for business to know how well they performed.