COMMERCE 1AA3 Lecture Notes - Lecture 4: Cash Flow Statement, Cash Cash, Cash Flow

18 May 2016

School

Department

Course

Professor

Document Summary

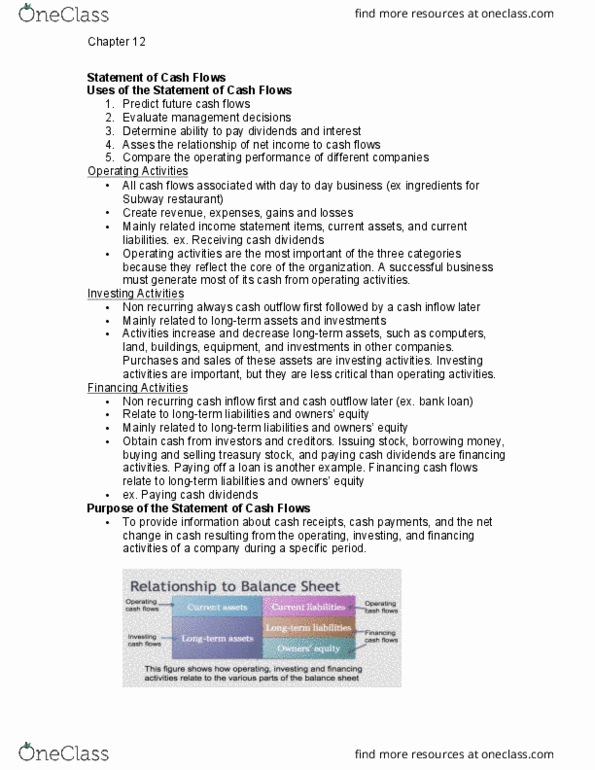

Predicts future cash flows: past cash receipts and payments. Evaluates management decisions: how managers got their cash, how cash was used to run the business. Determines ability to pay dividends and interest: shows ability to make these payments. Shows relations of net income to cash flows: but cash flow can suffer even when net income is high. Highly liquid short term investments: easily converted into cash with little delay, e. g. Operating: create revenue, expenses, gains and losses (net income) Related to lo(cid:374)g te(cid:396)(cid:373) lia(cid:271)ilities a(cid:374)d ow(cid:374)e(cid:396)s" equity. Operating cash flows: current assets, current liabilities. Financing cash flows: long-term liabilities, sto(cid:272)kholde(cid:396)s" e(cid:395)uity. Indirect: reconciles from net income to net cash provided by operating activities. Direct: reports all cash receipts and cash payments from operating activities. Investing and financing cash flows are the same as indirect method: adjusting income statement items from accrual to cash basis. Positive items: net income, depreciation and amortization expense, losses on sales of long term assets.