COMMERCE 1BA3 Lecture Notes - Lecture 4: Deferral, Current Liability, Working Capital

19 Sep 2013

School

Department

Course

Professor

Document Summary

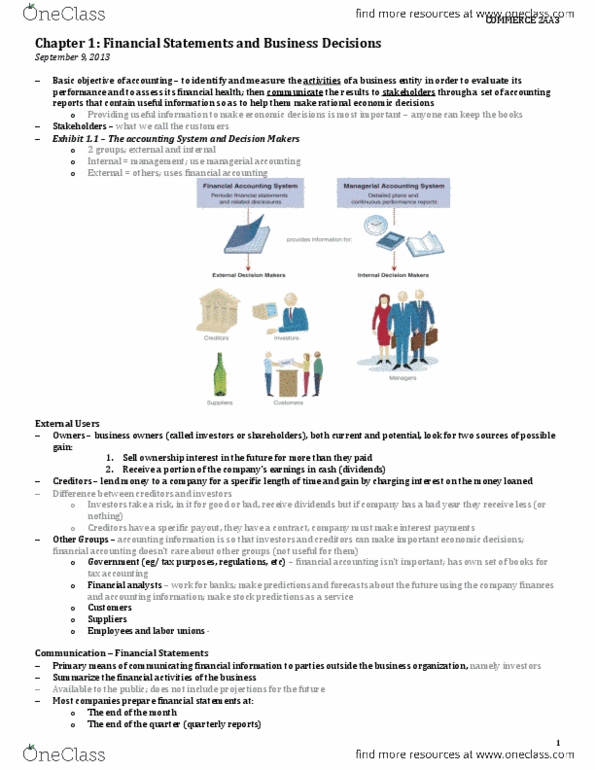

Chapter 2: investing and financing decisions and the statement of financial. Framework that informs accounting practice; issue at a business, consult conceptual framework for solution. Eg/ future cash flows million; but risk/uncertainty is that this cash high (probability 1/1 million (like the lottery)) high uncertainty, cannot plan future on this future cash flow: eg/ next paycheck. Uncertainty low; can depend on receiving it: eg/ proceeds from the sale of house. Timing 90% of houses sell within the first 3 months of listing. Amount a 10% range around the asking price. Qualitative characteristics what are the qualities that accounting must have to be useful. Elements of statements what accountants measure; what information it provides. Recognition and measurement criteria : eg/ business buys a car; recognize as an asset? (recognition; yes); how much should they put in the books? (measure; however much they paid) Qualitative characteristics of accounting information: fundamental qualitative characteristics, relevance in order to be relevant, it must be: