COMMERCE 1BA3 Lecture Notes - Promissory Note, Cash Flow, Interest Expense

19 Nov 2013

School

Department

Course

Professor

Document Summary

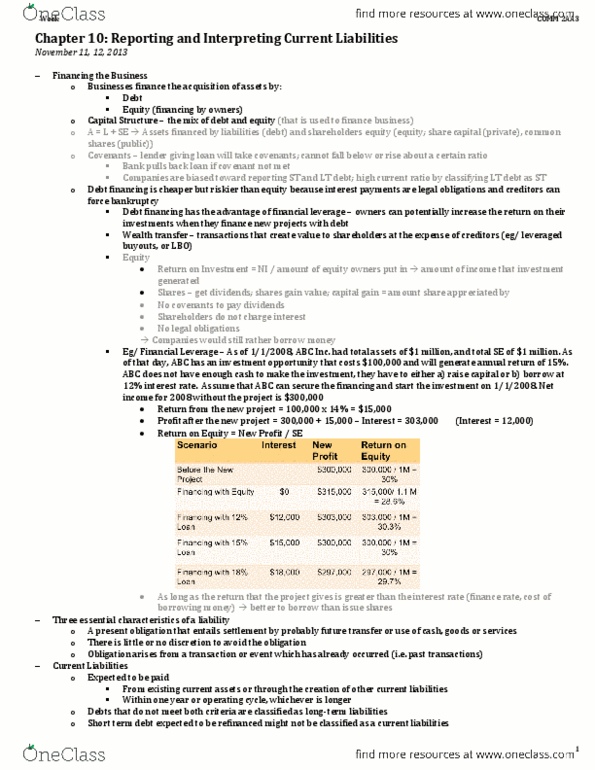

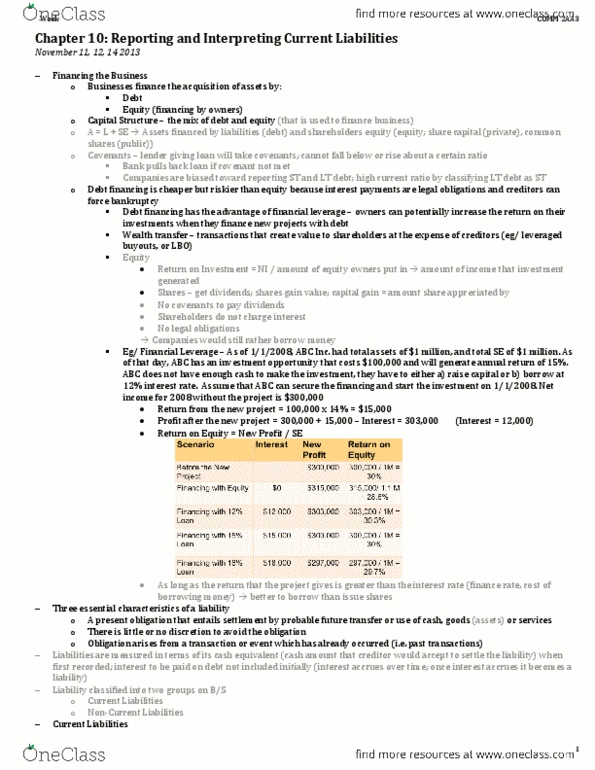

Capital structure long-term debt: long term debt can be in the form of notes payable, bonds payable, lease obligations and mortgage payable. Advantages of bonds: bonds are debt, not equity, so the ownership and control of the company are not diluted, cash payments to the debt holders are limited to the scheduled payments of interest principal. Compared to when shareholders do not get return on equity (ni/shareholders equity) can lead to problems. Dividends come after ni on statement of changes in equity not tax deductible: positive financial leverage. Increase return to shareholders at the expense of your creditors; cheaper to finance with debt than equity . Disadvantages of bonds: risk of bankruptcy exists because the interest and principal are legal obligations and must be paid back as scheduled or creditors will force legal action. Secured backed up by collateral; money lent is backed up; reserves kept by company in case money is lost.