COMMERCE 1BA3 Lecture Notes - Market Rate, Interest Expense, Promissory Note

30 Nov 2013

School

Department

Course

Professor

Document Summary

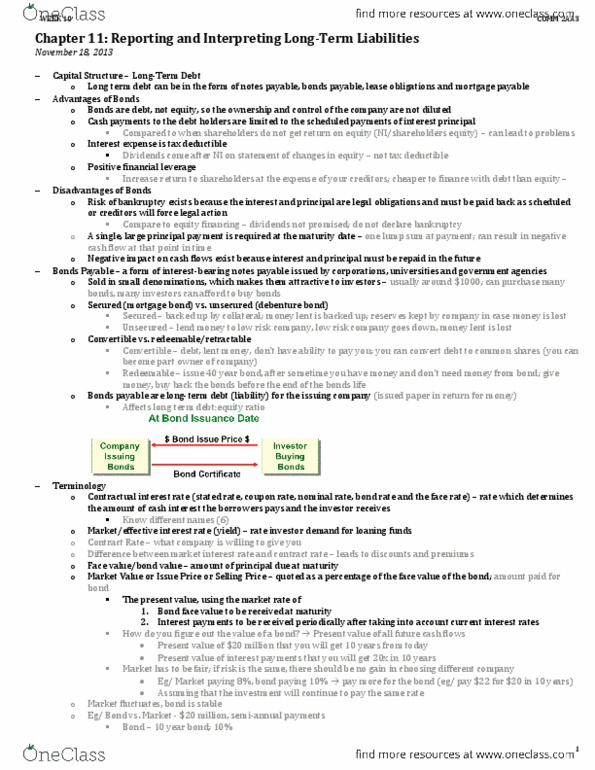

Long-term debt can be in the form of: notes payable, bonds payable, lease obligations, mortgage payable. This chapter will focus on bonds payable. Bonds are debt not equity so do not lose ownership or control of company. Cash payments to debt holders are limited to scheduled payments of interest principal (do not have to pay dividends) Risk of bankruptcy exists because interest and principal are legal obligations (must be paid back as scheduled or creditors will for legal action) Huge lump sum of money due when bond expires (may not have enough cash on hand at that time to pay it off) Negative impact on cash flows exists because interest and principal must be repaid in future. Advantages of bonds are advantages of any debt financing over equity financing. Financial leverage: being able to increase return on equity. Form of interest-bearing notes payable issued by corporations, universities and government agencies. Sold in small denominations (makes them attractive to investors)