COMMERCE 1BA3 Lecture Notes - Cash Advance, Asset, The Travelers Companies

26 Feb 2014

School

Department

Course

Professor

Document Summary

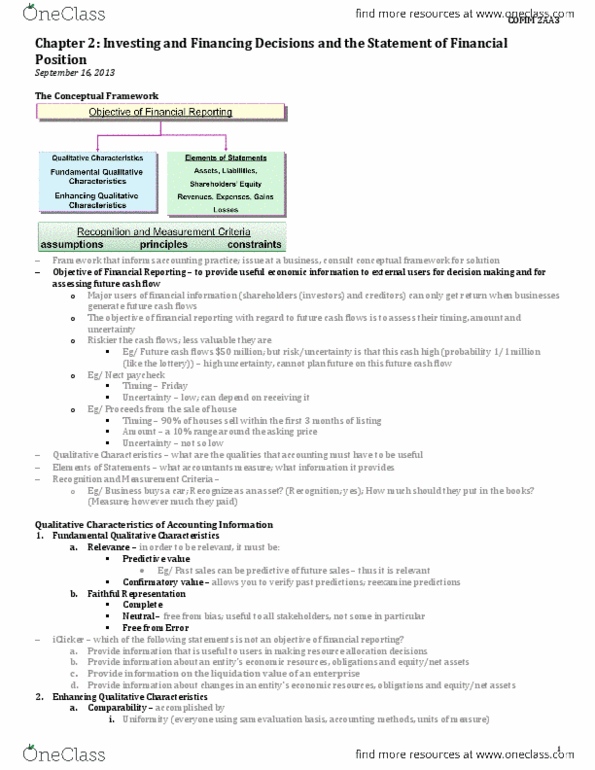

Investing and financing decision and the balance sheet. Identify the qualities that make accounting information useful. Describe and define the balance sheet and its major elements. Understand alternative methods of measuring the value of assets. Understand the disclosure rules of assets in the balance sheet. Understand alternative methods of measuring the value of liabilities. Understand the disclosure rules of liabilities in the balance sheet. Identify and calculate ratios for analyzing a company"s profitability. Identify and calculate ratios for analyzing a company"s liquidity and solvency. The conceptual framework of accounting is a set of objectives, principles, and guidelines that help. The highest level of the conceptual framework is the objective of financial reporting. The objective of general purpose financial reporting is to provide financial information about the reporting entity that is useful to existing and potential investors, lenders and other creditors in making decisions about providing resources to the entity.