COMMERCE 2AB3 Lecture Notes - Lecture 2: Finished Good, Fixed Cost, Cost Driver

26 Jun 2018

School

Department

Course

Professor

CHAPTER 2 – CLASS NOTES

3 CLASSIFICATIONS OF COST

BEHAVIOUR TRACEABILITY

How can it be traced?

FUNCTION

Why are you spending

money?

VARIABLE BEHAVIOUR

(UVC, UTC)

DIRECT COST

Can be economically traced to the cost object

(the item being produced)

Ex. The CEO of Toyota's salary is direct or indirect to Toyota.

Direct - there's a certain salary that the CEO gets regardless of

the models that are sold.

PRODUCT PURPOSE

(Production)

- Product cost

(inventoriable cost):

Assets, goes in a

balance sheet. When

sold they will go in the

COGS of the Income

Statement.

FIXED BEHAVIOUR

(UFC, FTC)

INDIRECT COST

- Selling cost or it is not economically feasible

to trace the cost object.

- They must be ALLOCATED, ASSIGNED, or

CHARGED to the cost object using a cost

allocation base (cost driver).

Ex. Utilities, cleaning supplies, water usage,

etc.

(Harder to track)

Ex. CEO of Toyota's salary is direct or indirect in respect to

the Corolla model?

Indirect - the CEO works for a company which has many

models, so we don't know how much of his time is spent on

what model. We can't trace the salary back to a particular

model.

PERIOD PURPOSES

(Selling)

- Selling costs, they are

expenses, and go in the

Income Statement.

COMPLICATIONS

Gas Rent

Variable

Unit Variable

Cost = $1/Liter

= Fixed

Fixed

$500 rent for room

for 1 hour.

Unit fixed cost for 1

student: $500

2 students: $250

= Variable

Total Variable

Cost for Gas:

1L = $1

20 L = $20

Total Fixed Cost

$500

Therefore, fixed costs and

variable costs are only defined

in totality.

Ex. If I want to find out how much DeGroote

should contribute to the profs salary, is it clear,

can it be traced? Yes! There's a fixed salary for

hours and courses taught.

Other things are harder to trace: Ex. The Podium:

the cost of wood, nails, tablet etc. It wouldn't be

worth it to calculate the cost of all the little objects

that make it up. It is purposely made indirect,

because we don't want to bother tracking the cost

of making each podium since some may have cost

more than others depending on the price of the

materials.

Unit Variable Cost (UVC)- has value when expressed.

find more resources at oneclass.com

find more resources at oneclass.com

Unit Fixed Cost (UFC) - useless, unless coupled with a denominator.

Denominator Level - cost allocation base/capacity

oEx. Unit fixed cost for rent is $50 if 10 students come to class, so when

5 students come it's $100.

oWhy is it $50 per student? 10 students is the denominator level.

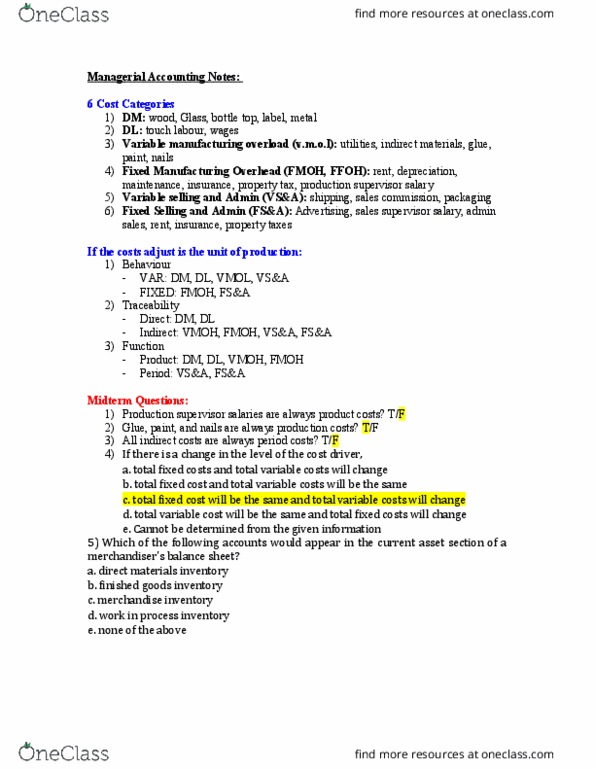

PRACTISE QUESTIONS

TRUE OR FALSE

1. All direct costs are always production costs.

TRUE – Sales Salaries cannot be tracked.

2. All fixed costs are product costs.

FALSE – Rent is split between production and what is for rent. Some costs

can be selling costs.

3. Direct materials are variable, direct, and product costs.

TRUE – It is a variable because if I’m using 1kg of wood for one table, then for

2 tables I would use $200 etc.

4. All indirect costs are always period costs.

FALSE – We can’t track an indirect cost, but we don’t know if it’s for

production or selling (Ex. Rent is split between production & selling).

January 11, 2015

CH. 1,2: HOMEWORK PRACTISE

1. Variable Cost Per Unit – fixed

So it can’t be a and d

E (None of the above) is never an answer

B) Fixed cost per unit increases as production decreases

The rent per student increases as # of students decreases

5. Change in level of cost driver,

c) Because fixed costs are fixed in total, and variable costs are variable in

total.

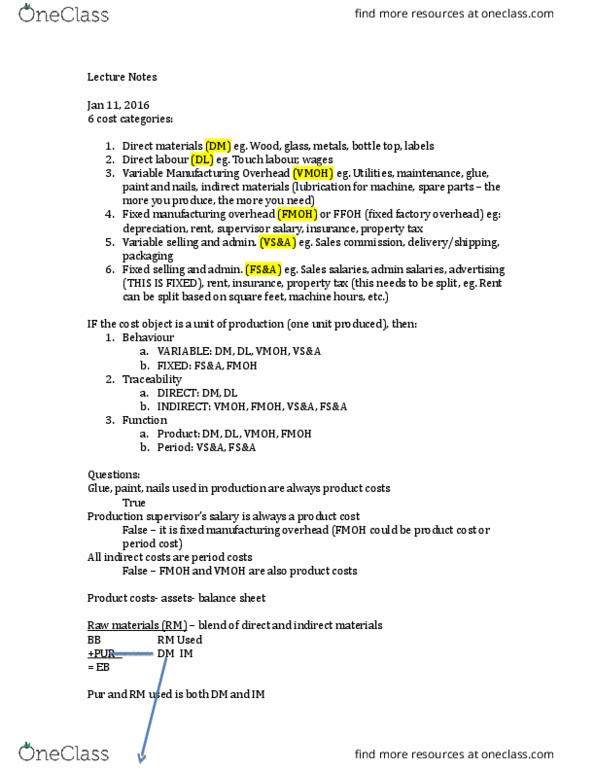

6 COST CATEGORIES

1. Direct Materials (DM) Wood, Glass, Bottle, Top, Label, Metal

2. Direct Labour (DL) Touch Labour (people who make the units), Wages

3. Variable

Manufacturing

Overhead (V.M.O.M)

Utilities (the more you produce, the more you will

incur, but there’s no way to track it to the product),

Maintenance of the Machines, Indirect Materials, glue,

paint, nails (the more you produce, the more you need)

4. Fixed Manufacturing

Overhead (FMOH)

Rent, Depreciation, Spare Parts, Maintenance,

Insurance, Property Taxes, Production Supervisor

Salary

5. Variable Selling and

Admin (VS&A)

Shipping, Sales Commissions, Packaging.

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Selling costs, they are expenses, and go in the. Can be economically traced to the cost object (the item being produced) The ceo of toyota"s salary is direct or indirect to toyota. Direct - there"s a certain salary that the ceo gets regardless of the models that are sold. Selling cost or it is not economically feasible to trace the cost object. Charged to the cost object using a cost allocation base (cost driver). Utilities, cleaning supplies, water usage, etc. (harder to track) Indirect - the ceo works for a company which has many models, so we don"t know how much of his time is spent on what model. We can"t trace the salary back to a particular model. There"s a fixed salary for hours and courses taught. The podium: the cost of wood, nails, tablet etc. It wouldn"t be worth it to calculate the cost of all the little objects that make it up.