COMMERCE 2AB3 Lecture Notes - Lecture 19: Finished Good, Indirect Costs

Document Summary

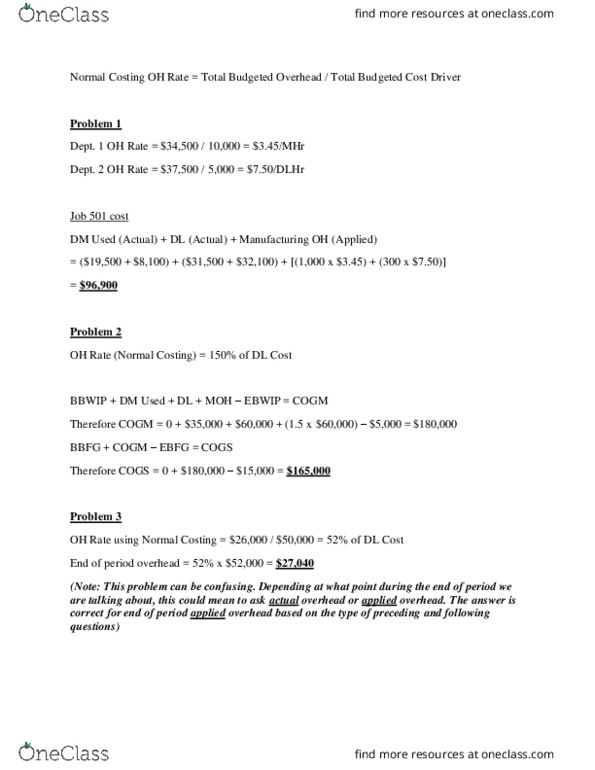

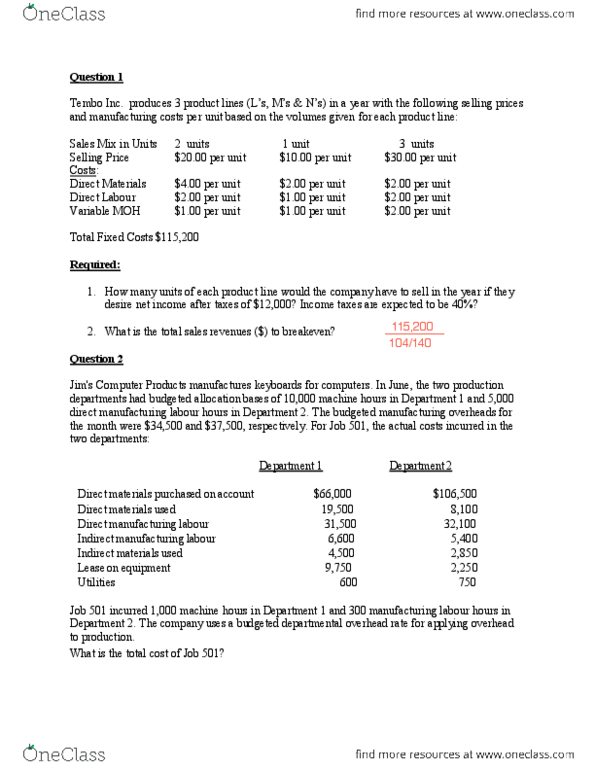

In june, the two production departments had budgeted allocation bases of 10,000 machine hours in department 1 and 5,000 direct manufacturing labour hours in. The budgeted manufacturing overheads for the month were. For job 501, the actual costs incurred in the two departments: Job 501 incurred 1,000 machine hours in department 1 and 300 manufacturing labour hours in department 2. The company uses a budgeted departmental overhead rate for applying overhead to production. The bce company allocated manufacturing overhead using a predetermined overhead rate of 150% of direct manufacturing labour. The records show the following for the period: Work-in-process control - ending inventory = $ 5,000. Finished goods control - ending inventory = ,000. There were no beginning inventories of work-in-process or finished goods. The cost of goods sold for the period using normal costing would be: The dawson company uses normal costing with the indirect costs being allocated based on the direct manufacturing labour costs.