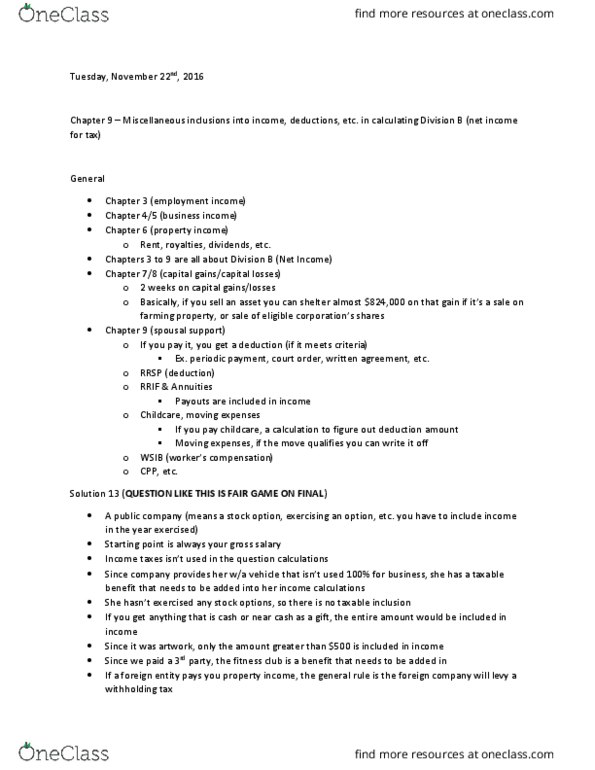

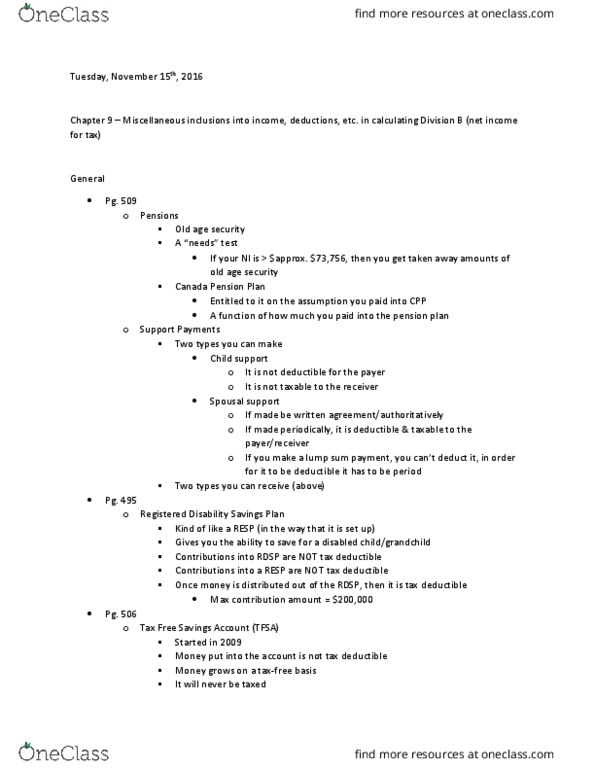

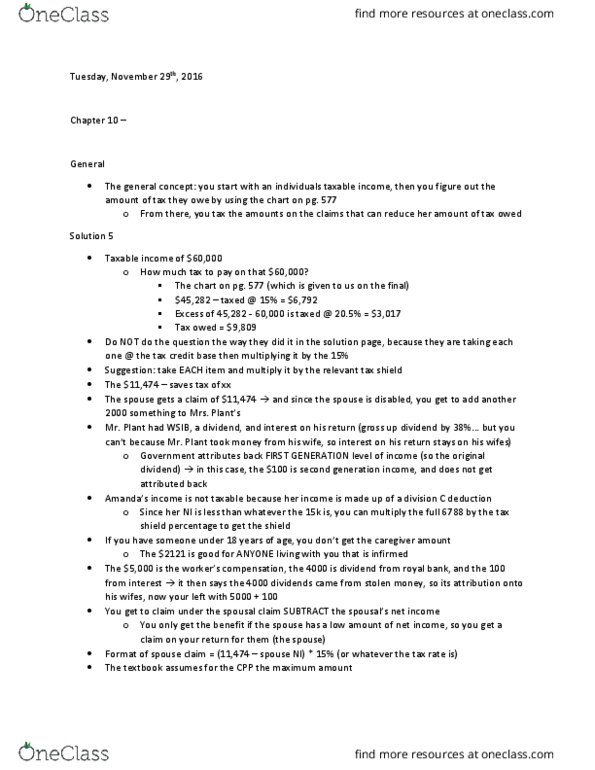

COMMERCE 4SD3 Lecture Notes - Lecture 7: Property Income, Tax Bracket

Document Summary

General rule: property income = rents, royalties, interest, & dividends, this is a return on invested capital, it"s (cid:272)o(cid:374)sidered passive/property income, size of organization constitutes if its business income, or property income. Earn-outs: things based on production/use of the asset, this is now property income (income under 12. 1. g) Solution 3 (a) the ,000 payment for fixed assets (there is going to be a terminal loss, going to need to recapture: no clue what the undepreciated capital cost is. If you sell ,000 you get 25k, if you sell sh, you get sh. It"s (cid:374)o(cid:449) (cid:272)o(cid:374)sidered full(cid:455) ta(cid:454)a(cid:271)le u(cid:374)der (cid:1005)(cid:1006) (cid:894)(cid:1005)g(cid:895) (d) If you pay yourself a salary = business deductible expense (a salary is a pre- If you leave profits in the incorporated company, you will defer the amount of tax you need, therefore paying much less on tax than you needed to.