ECON 1B03 Lecture Notes - Lecture 8: Economic Equilibrium, Perfect Competition, Marginal Revenue

17 views1 pages

31 Mar 2016

School

Department

Course

Professor

46

ECON 1B03 Full Course Notes

Verified Note

46 documents

Document Summary

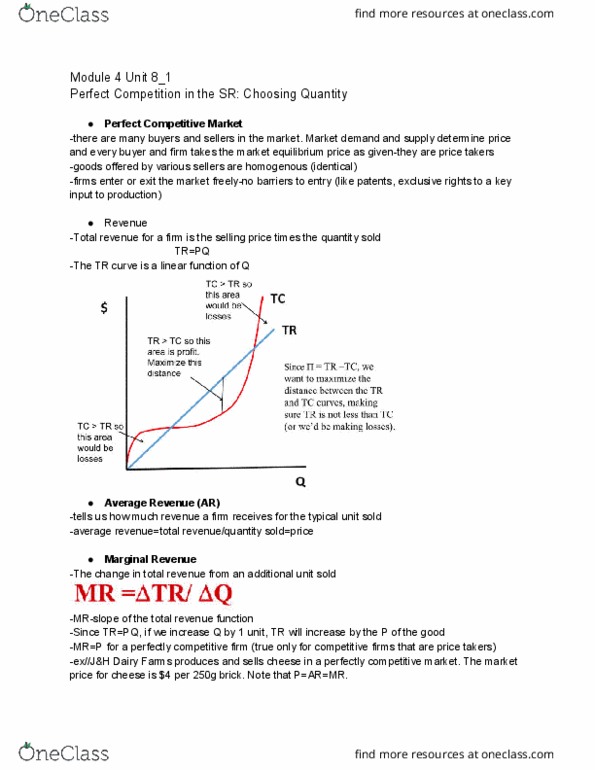

Many buyers and sellers in the market. Market demand and supply determine price and every buyer and firm takes the market equilibrium price as given they are price takers. The goods offered by various sellers are homogenous. Firms can freely enter or exit the market. Tells us how much revenue a firm receives for the typical unit sold. Ar = tr / q = pq / q = p. The change in tr from an additional unit sold. Mr = delta tr / delta q. Mr is the slope of the tr function. Since tr = pq, if we increase q by 1 unit, tr will increase by the p of that good. Mr = p (for a perfectly competitive firms that are price- takers) If we know a firm"s tc of producing at each of the q levels. Can easily calculate profit: pi = tr tc.

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers