ECON 1B03 Lecture Notes - Lecture 8: Marginal Cost, Marginal Product, Marginal Revenue

31 May 2016

School

Department

Course

Professor

46

ECON 1B03 Full Course Notes

Verified Note

46 documents

Document Summary

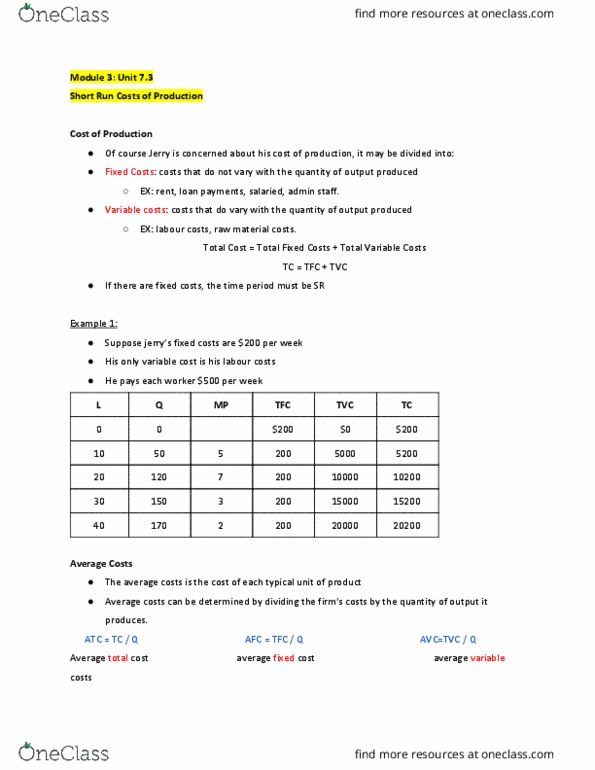

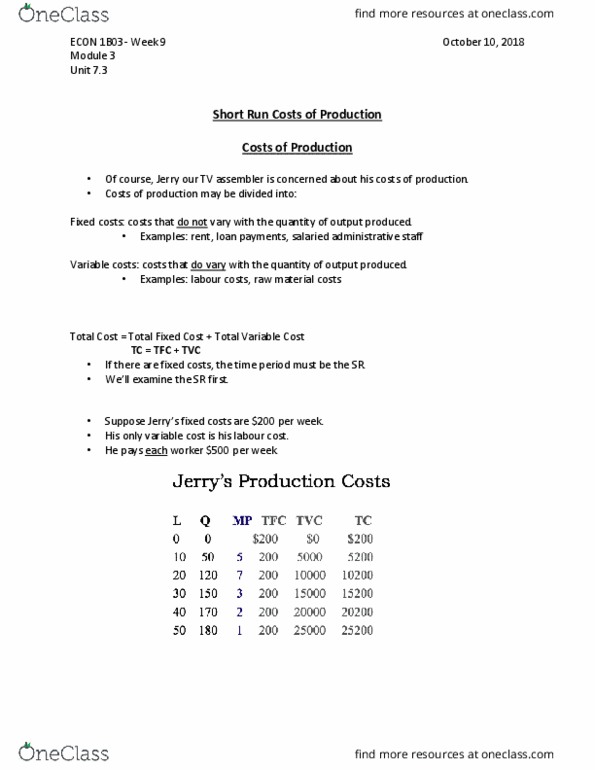

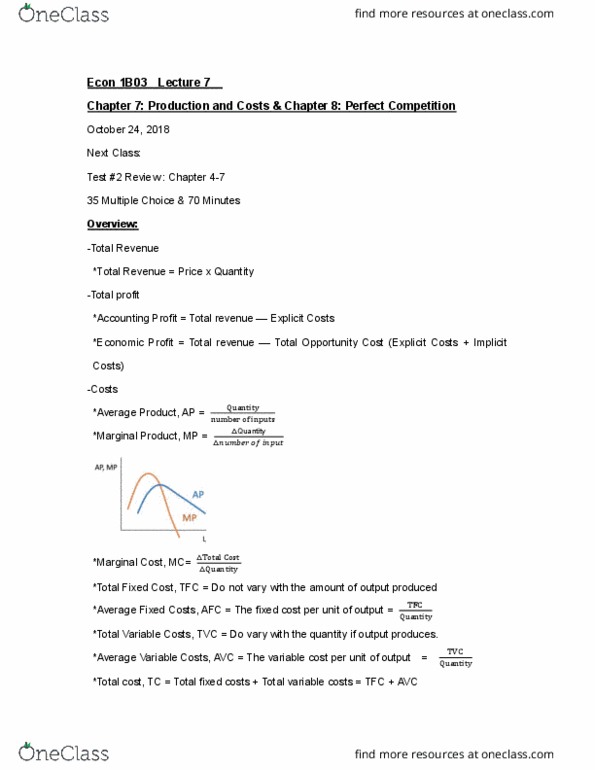

Information: the quantity of output to supply, how to produce that output, the quantity of each input to demand, the price of output, techniques of production available, the price of inputs. Two conditions hold in the short run: fixed factor of production, firms can"t enter/exit. Fixed costs are those that a firm bears in the short run that doesn"t depend on its output level. Incurred even if the firm is producing nothing. No fixed costs in the long run. Variable costs are any that a firm bears that depends on the level of production chosen. Total costs are fixed costs plus variable costs. Include heating, lease payments, insurance, taxes, etc. Certain forms of capital can be variable in the short run (employees, computers, etc. ) Firms have no control over fixed costs in the short run. Is the total fixed cost divided by the number of units of output (q)