ECON 2X03 Lecture Notes - Mpeg-1 Audio Layer I, Fixed Cost, Isoquant

10 Apr 2013

School

Department

Course

Professor

Document Summary

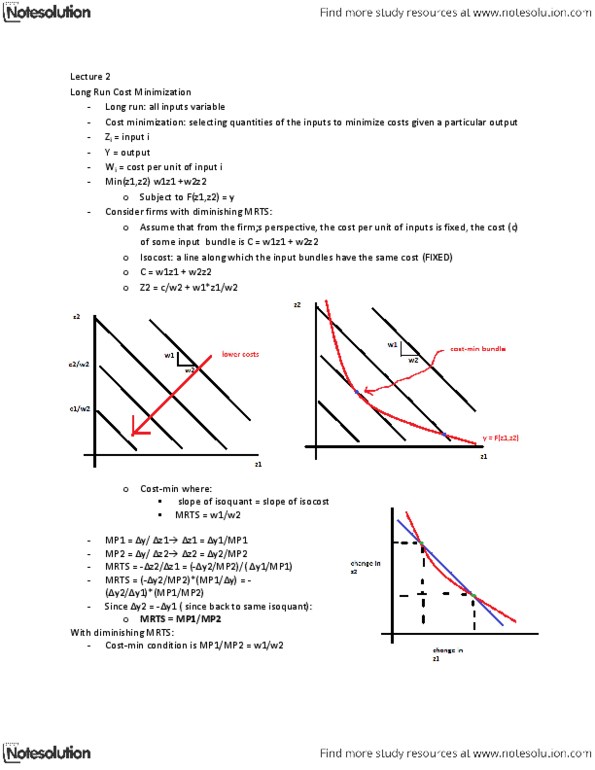

Inputs (factors or factors of production): things firms use to make their output. Input bundle: a list of quantities, one for each input a firm can use. Production function: the maximum output a firm can produce as a function of input bundles y = output z = input. So a production function ex: y = f(z1,z2) Assume firms behave in such a way to maximize profits (difference between revenue and cost of production) Given that revenue depends on output, profit maximization, requires that the given level of output be produced at a minimum cost. The firm"s cost minimization problem: min w1z1 + w2z2 subject to f(z1z2) > y" where: W1 = cost per unit of input 1. W2 = cost per unit of output 2. Opportunity cost (economic cost or cost): the opportunity cost of something is the value he value of the resources used to obtain it in their best alternative.