COMM 329 Lecture Notes - Lecture 14: Prepayment Of Loan, Yield Curve, Credit Risk

29 Aug 2016

School

Department

Course

Professor

Document Summary

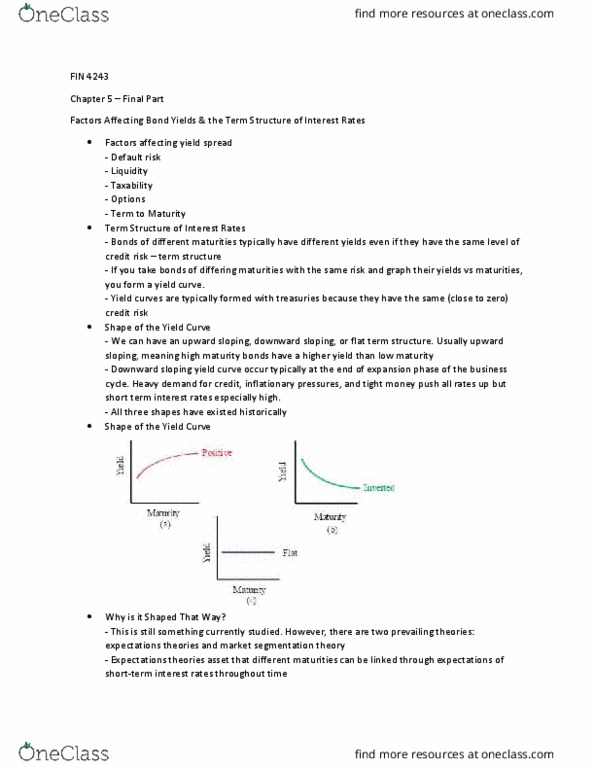

A graphical depiction of the prevailing yields, at any given point of time, on a set of bonds that differ from one-another only in terms to maturity. New information is known with certainty and is immediately priced into a market. For bond markets specifically this new information is likely interest rates, i think. Interest rates prevailing today on loans to be made in the future. A proxy for the consensus market"s expectation of future spot ratesm. Reasons why the pure expectation theory breaks down: Interest rates are serially correlated [autocorrelation, t ~ f(t-1)] 1: most investors are not risk neutral. Pure expectation theory: zero-coupon rates, in equilibrium, will be equal to the geometric mean of the sequence of expected future short-term, zero-coupon rates over that period. (1 + r2)^2 = (1 + r1)(1 + f1,2) Biased expectation theory: spot-yields are seen as the sum of the geometric mean of the present/expected future short-term rates and a term premium .