ACC 100 Lecture Notes - Lecture 6: Quality Management, Cost Driver

21 Apr 2016

School

Department

Course

Professor

Document Summary

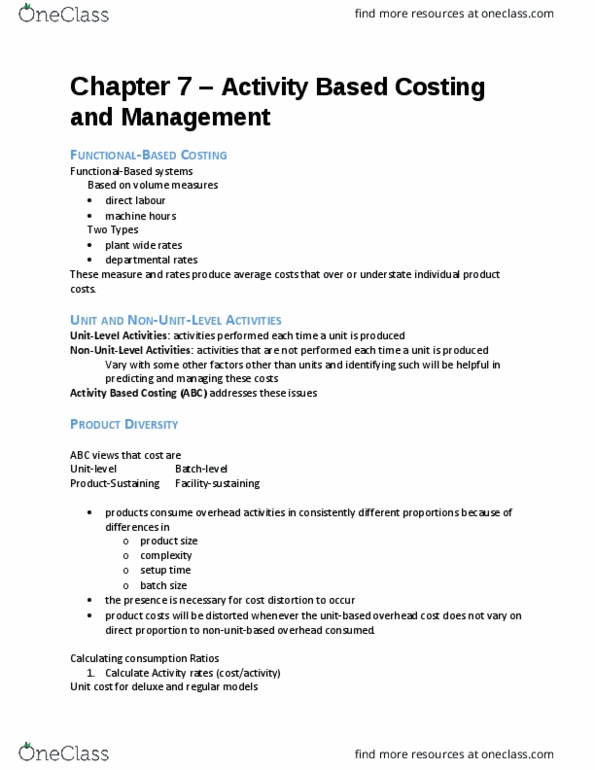

Better allows firms to trace the profitability for each product or service. Allows for betting tracking of consumption of a company shared resources among different products and customers. Helps turn overhead costs that are indirect under traditional costing methods into direct costs under abc costing. Allows for inexpensively tracking many activities" and their costs. All products consumer resources in a similar manner. The cost of developing individual cost pool was to great. The cost of tracking appropriate cost drivers was too great. Resistance within the company was too great and would cause dissention amount managers. Top managers could not be convinced to support the project. Quality: doing it right the first time. Can improve profitability in two ways: (1) increase customer demand which increase revenue, (2) by decreasing costs. Costs of quality: activities performed because poor quality may or does exist: control activities: performed by an organization to prevent or detect poor quality, failure activities.