ACC 406 Lecture : Profit Planning

17 May 2011

School

Department

Course

Professor

Document Summary

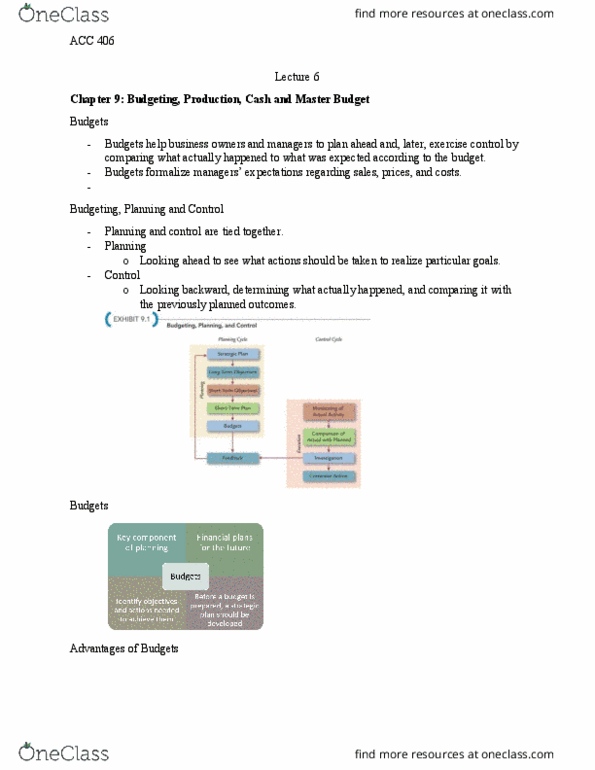

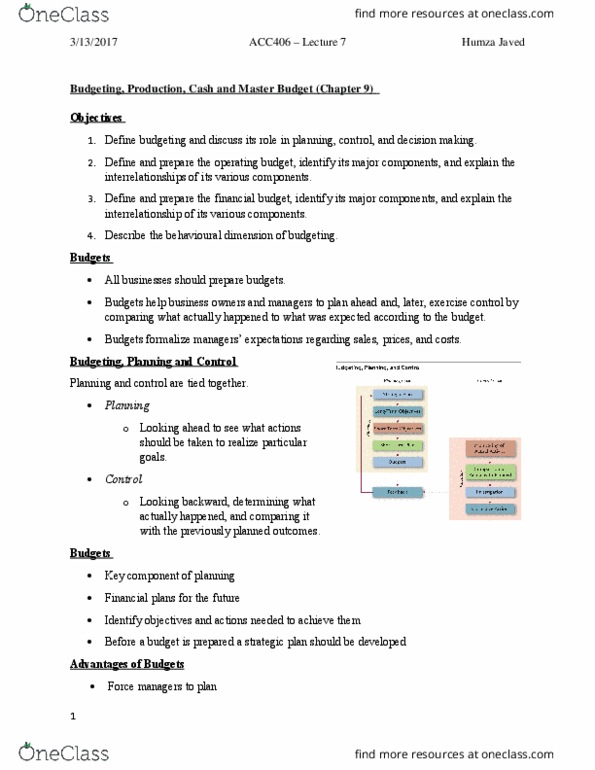

Chapter 9 budgeting process of preparing budgets. Types of budgets: operational budget, sales budget how many units to be sold (determines production budget, production budget how many units to be produced (determines input. direct material purchases budget estimates direct materials cost. direct labor budget estimates direct labor cost. overhead budgets estimates overhead cost: financial budget, cash budget estimates cash in/outflow (receipt/payments, projected income statement estimate revenue and expenses, projected balance sheet. 60% collected in the same month of sale. 50% without cash discount: cost-to-sales ratio: 22:1. Monthly ending inventory equal to coming month"s production requirements. Purchase for july sales (1,140,000 * 0. 22) = ,800. Less: beginning inventory (1,140,000 * 0. 22) = ,800.