ACC 406 Lecture Notes - Lecture 8: Minivan, Corn Chip

17 Apr 2016

School

Department

Course

Professor

Document Summary

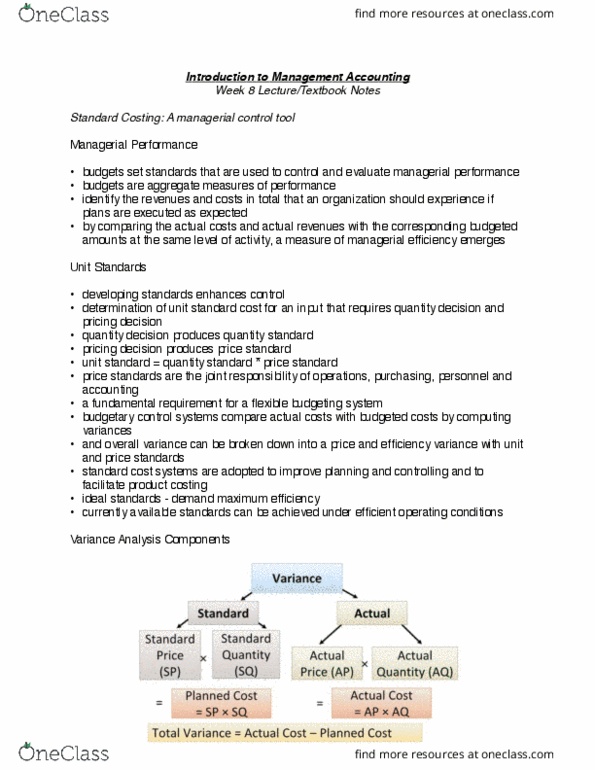

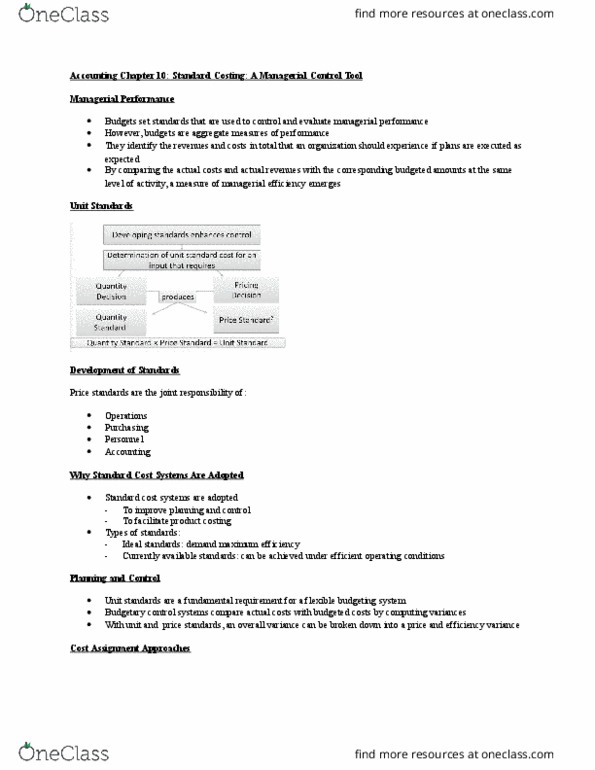

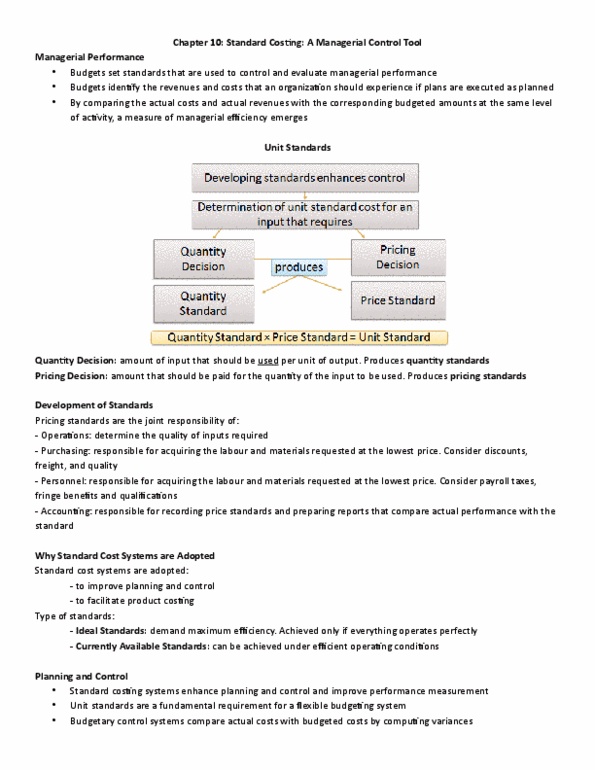

Chapter 10 standard costing: a managerial control tool. Budgets set standards that are used to control and evaluate managerial performance. They identify the revenues and costs in total that an organization should experience if plans are executed as expected. By comparing the actual costs and actual revenues with the corresponding budgeted amounts at the same level of activity, a measure of managerial efficiency emerges. Quantity standard: the amount of input that should be used per unit of output. Price standard: the amount that should be paid for the quantity of input to be used, joint responsibility of operations, purchasing, personnel and accounting. Unit standard: quantity standard x price standard, used to enhance cost control, budgeted unit" costs. Types of standards: ideal standards demand maximum efficiency, currently available standards can be achieved under efficient operating conditions and offer the most behavioural benefits. Unit standards are a fundamental requirement for a flexible budgeting system.