ACC 410 Lecture Notes - Iunit

18 Apr 2011

School

Department

Course

Professor

Document Summary

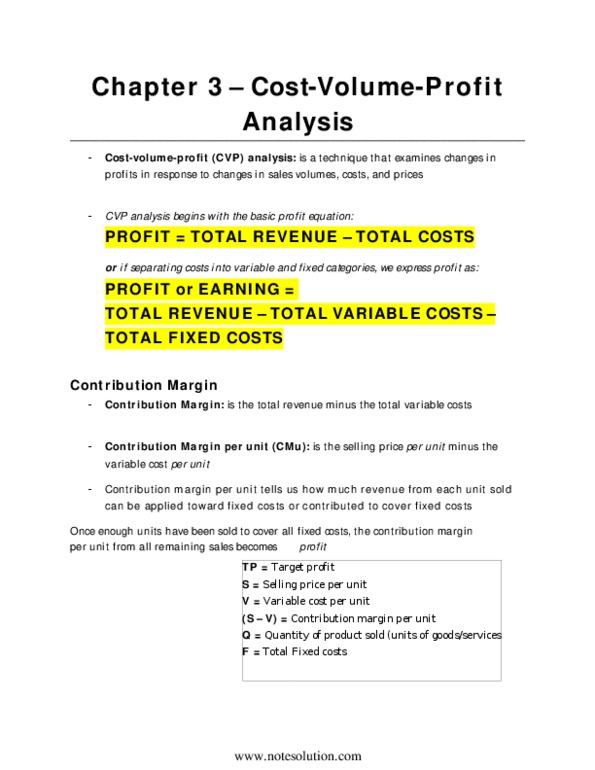

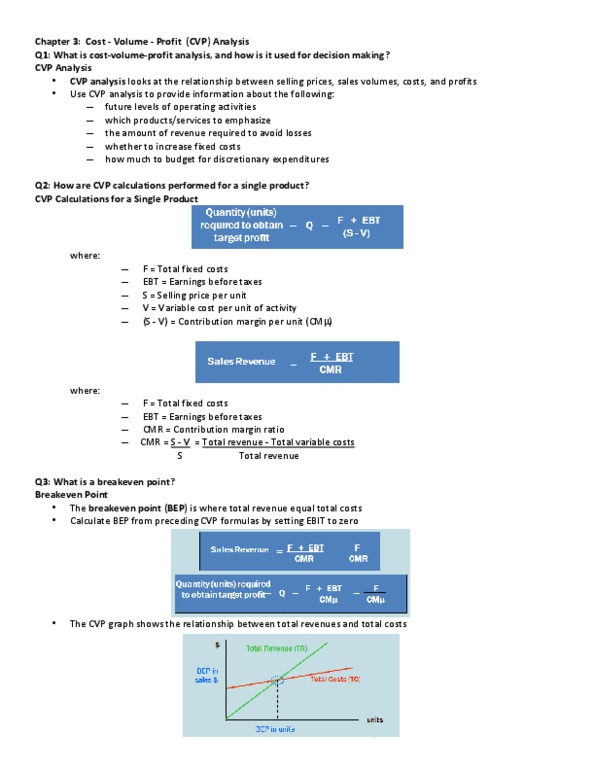

Cost-volume-profit (cvp) analysis examines relationship between selling prices, sales volumes, costs and profits. Used to provide information about: future levels of operating activities, which products/services to emphasize, the amount of revenue required to avoid losses, whether to increase fixed costs, how much to budget for discretionary expenditures. Contribution margin: cm = r v: tells us how much revenue from each unit sold can be applied toward fixed costs or contributed to cover fixed costs. Contribution margin per unit: cmu = su vu. Cvp analysis can be performed using either: units (quantity) of product sold, revenues (in dollars) Earnings (profit) equation: ebt = s * q v * q f = (s v) * q f. Contribution margin ratio (cmr) percentage by which selling price per unit exceed variable cost per unit, or contribution margin as a percentage of revenue. Breakeven point level of operating activity at which revenues cover all fixed and variable costs.