AFF 210 Lecture Notes - Lecture 3: Income Statement, Current Liability, Financial Statement

25 Mar 2016

School

Department

Course

Professor

Document Summary

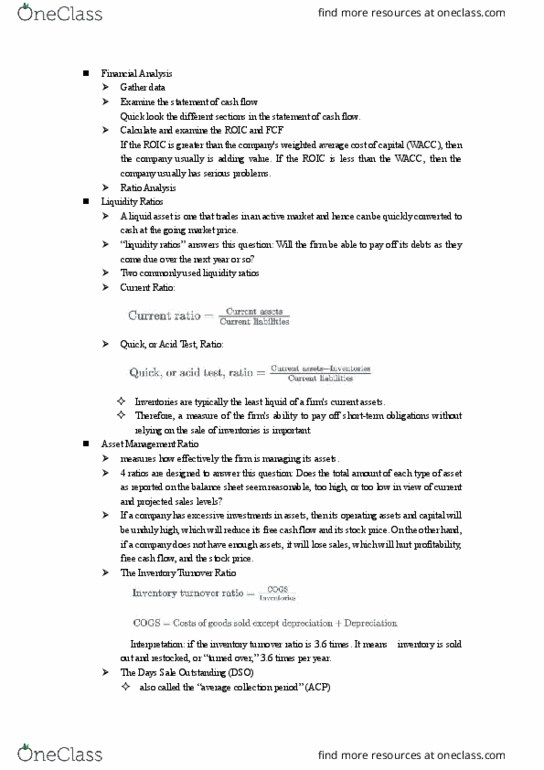

Ratio analysis financial ratios extract important information that may not be obvious by examining a firm"s financial statements financial ratios remove the size factor between different firms & make comparison meaningful. Quick/acid test ratio = current assets inventories/current liabilities. Minus inventories from current assets because losses are more likely to occur from inventories in case of bankruptcy. Debt management ratios examines the extent to which a firm uses debt financing/ financial leverage (lower leverage is safer) Debt ratio = total liabilities/ total assets x 100% Debt-to-equity ratio = total debt / total equity. Times-interest earned ratio = ebit/interest charges (measures the ability to pay interest) Ebitda coverage ratio = ebitda + lease payments/interest + principal. Payments+ lease payments (measures the ability to service debt) Days sales outstanding (dso) = a/r divided by sales/365. Dso represents the average length of time the firm must wait after making a sale and before receiving cash.