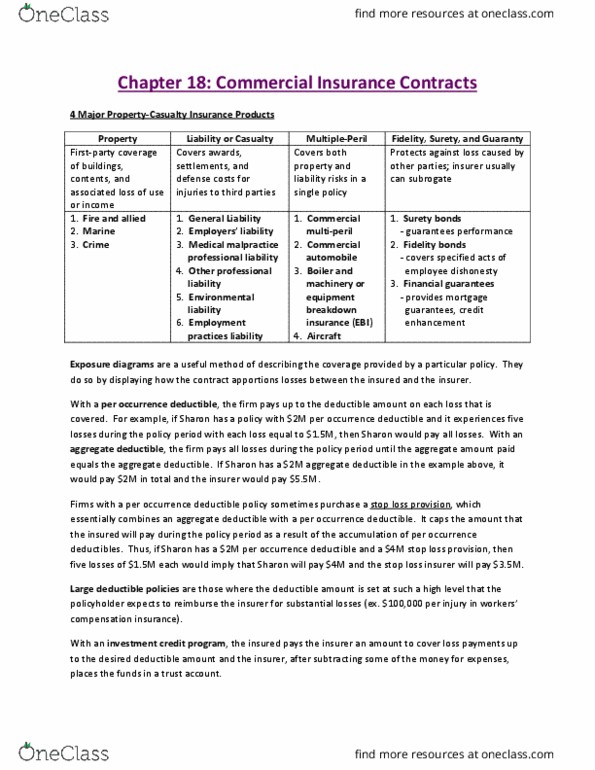

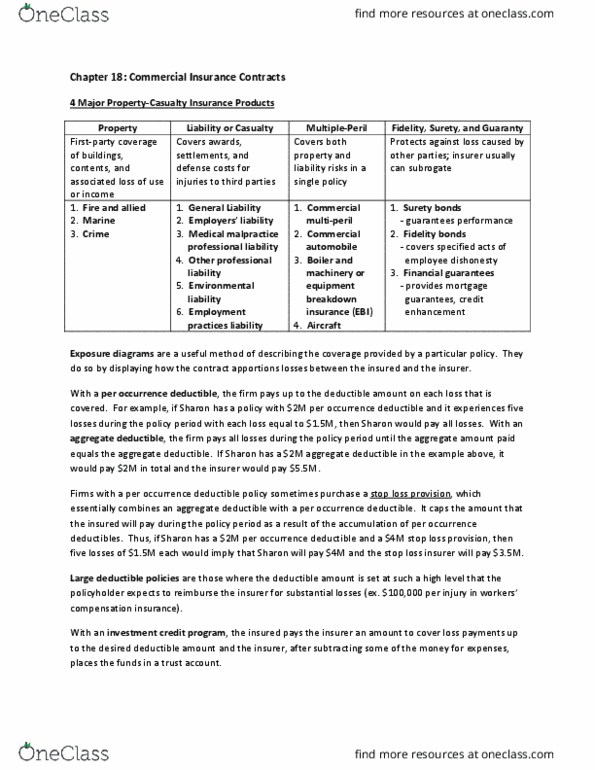

FIN 512 Lecture Notes - Lecture 5: Liability Insurance, Property Insurance, Side Effect

Two basic categories of commercial insurance:

- Property insurance

- Liability insurance

3 categories of commercial liability insurance:

- General liability

- Professional liability

- Employer liability

Bases to pay losses

- Occurrence policies

o Pay for losses that occurred during the policy period regardless of when the claim is

filled (ex. Drug company may get sued in the future for side-effect)

- Claims-made policies

o pay for losses after a certain date but the claims are made during the policy period

Aggregate deductible

- the firm pays all the losses for the year until the deductible limit is reached

Straight Deductible

- or per occurrence deductible – the firm pays the deductible for each separate loss

Franchise Deductible

- for marine, disappearing deductible

Self-insuring:

- the firm retains part of the risk exposure and usually has a fund set aside to cover losses.

- a deductible is called self-insured retention

Captives (2 types)

- Pure captives

o Insure only parents and parents subsidiaries

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Occurrence policies: pay for losses that occurred during the policy period regardless of when the claim is filled (ex. Drug company may get sued in the future for side-effect) Claims-made policies: pay for losses after a certain date but the claims are made during the policy period. Aggregate deductible the firm pays all the losses for the year until the deductible limit is reached. Or per occurrence deductible the firm pays the deductible for each separate loss. Self-insuring: the firm retains part of the risk exposure and usually has a fund set aside to cover losses. a deductible is called self-insured retention. Provides an additional dollar amount of coverage based on the underlying policy while the coverage of an umbrella policy goes beyond the scope of the underlying policy. Covers property and casualty in one contract. Someone who has temporary possession of property that belongs to another for storage, repair or servicing (dry cleaners, jewellers, laundries, repairs shops)