ECN 104 Lecture Notes - Lecture 9: Profit Maximization, Longrun, Personal Computer

22 Oct 2016

School

Department

Course

Professor

Document Summary

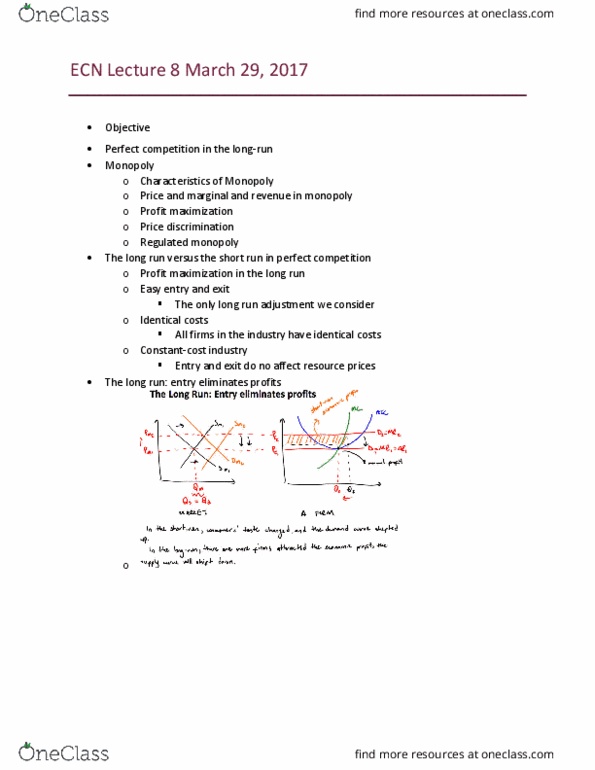

Ecn104 chapter 9: perfect competition in the long-run (lecture notes) The long run versus the short run in perfect competition: profit maximization in the long run. The only long run adjustment we consider. All firms in the industry have identical costs. Entry and exit do not affect resource prices. Temporary profits and the re-establishment of long-run equilibrium in a representative firm (panel a) and the industry (panel b) Temporary loss and the re-establishment of long-run equilibrium in a representative firm (panel: and the industry (panel b) Long-run supply for constant cost, increasing-cost, and decreasing-cost industries: constant cost industry. The long-run supply curve for a constant-cost industry is horizontal. The long-run supply curve for an increasing-cost industry is upward sloping. The long-run supply curve for a decreasing-cost industry is downwards sloping. In the long run, efficiency is achieved: productive efficiency. Dynamic adjustments: perfectly competitive markets will automatically adjust to: