ECN 104 Lecture Notes - Lecture 8: Opportunity Cost, Sunk Costs, Variable Cost

9 Nov 2017

School

Department

Course

Professor

Document Summary

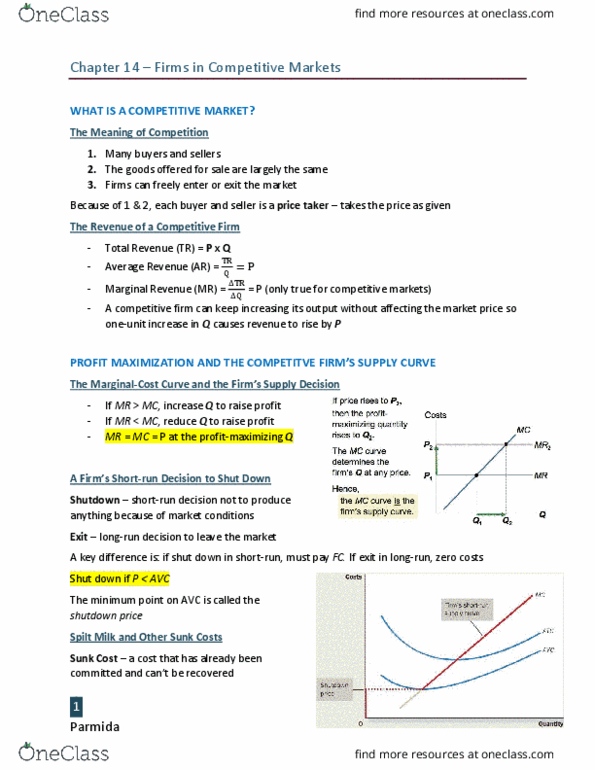

3 years after graduating, you run a business. You must decide how much to produce, what price and how many workers to hire. Demand is unlimited, your company is so small that no matter what quantity you produce, it will be sold. The firm is in a perfectly competitive market. Characteristics: many buyers and many sellers (everyone is the price taker, good offered for sale are alrgely the same, firms can freely enter or exit the market. Total revenue = price(fixed in the market) x quantity. Average revenue (ar) = total revenue / quantity = p. Marginal revenue (mr) = change in total revenue/ change in total quantity. Marginal revenue is equal to price for a competitive firm. A competitive firm can keep increasign its output without affecting the market price. Increase in one-unit in q causes revenue to rise by p, i. e, mr=p. *this is only true for firms in competitive markets.