ECN 104 Lecture Notes - Lecture 3: Deadweight Loss, Economic Equilibrium, Equilibrium Point

31 Mar 2016

School

Department

Course

Professor

Document Summary

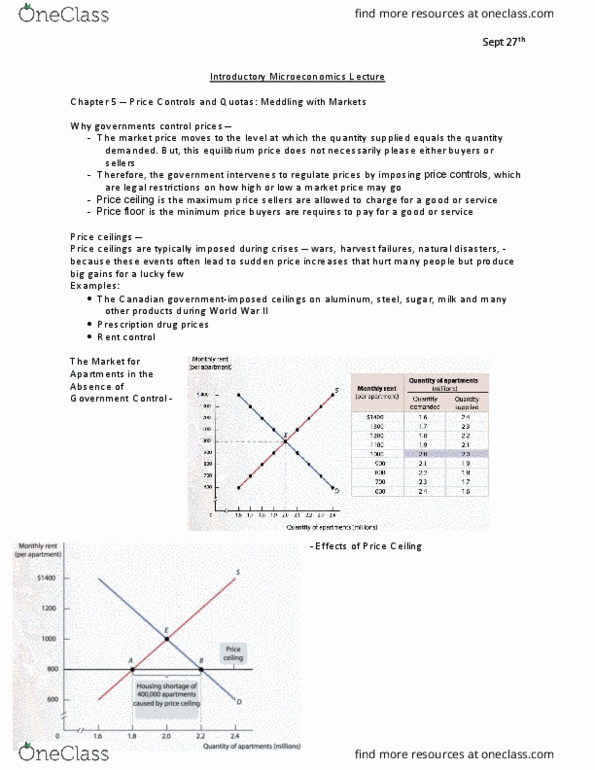

The market prices move to the level at which the quantity supplied equals the quantity demanded. But this equilibrium price does not necessarily please either buyers or sellers. Therefore the government intervenes to regulate prices by imposing price controls which are legal restrictions on how. They would rather favor one individual over the other. Price ceilings are typically imposed during crises, wars, harvest failures, natural disasters- because these events often lead to sudden price increases that hurt many people but produce bug gains for a lucky few. E. g. the canadian government imposed price ceilings on aluminum, steel, sugar, milk during world war ii. Causes shortages but not when the price ceiling is set at or above the equilibrium point. Inefficient allocation to customers: those who are willing to pay more for something and they need it more cant because of the price ceiling, and those who do not need the good as much may have the good.