HTA 602 Lecture Notes - Lecture 3: Accounts Receivable, Market Price, Asset Management

15 Apr 2018

School

Department

Course

Professor

Document Summary

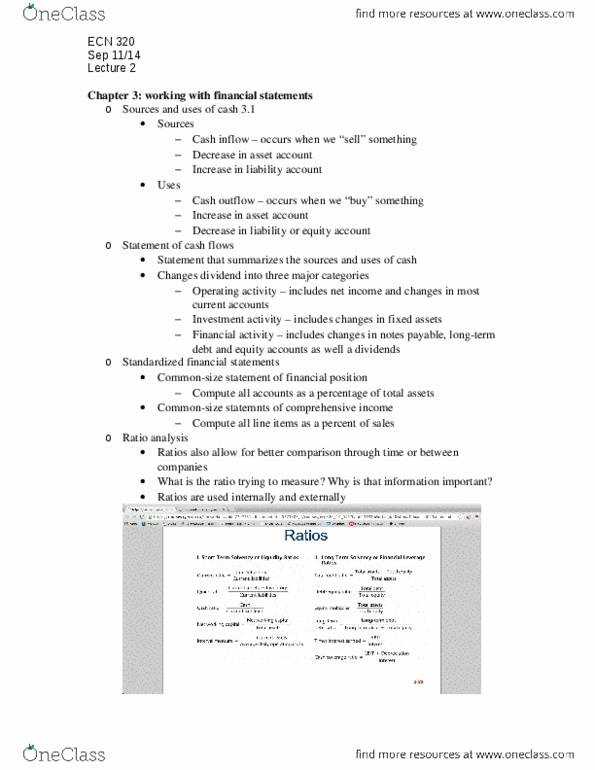

Statement that summarizes the sources and uses of cash. Changes divided into three major categories assets. Cash normally increases as: accounts receivable, inventory, prepaid expenses, accounts payable, accrued expenses. Current liabilities (cl) & cash move in the same direction. Ratios also allow for better comparison through time or between companies. As we look at each ratio, ask yourself what the ratio is trying to measure and why is that information important. Ratios are used both internally and externally. Short-term solvency or liquidity ratios interested in the cash of the business. Long-term solvency or financial leverage ratios life of the business (is the business going to keep going) Asset management or turnover ratio (how well are we using our assets) Profitability ratios (how much money are we making) Assume: market price = . 98 per share, shares outstanding = 205,838,910 = 2. 29. Eps = net income/shares outstanding: = 471, 916, 000/205,838,910 = 2. 29. Pe ratio = price per share/ earnings per share.