Business Administration - Financial Planning RFC122 Lecture Notes - Lecture 5: Tax Deduction, Small Business, Crystallization

25 Oct 2016

School

Professor

Document Summary

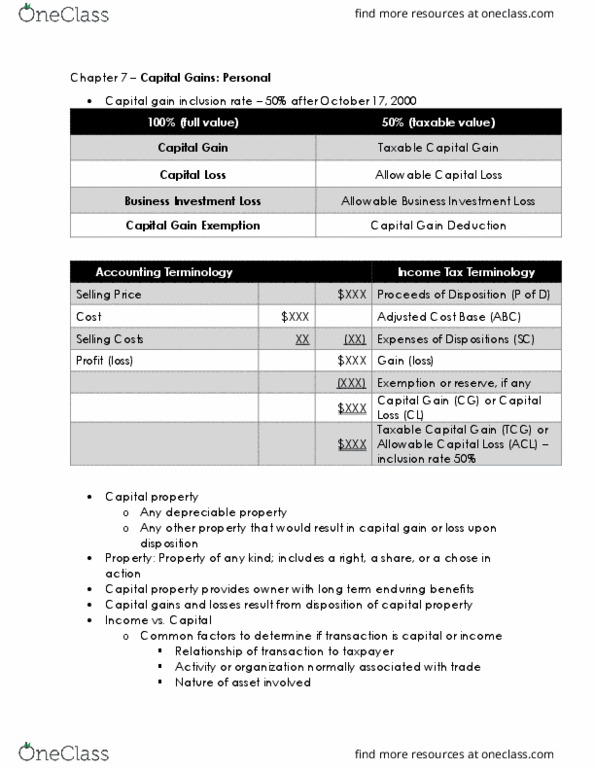

Rfc 122 chapter 6 in class notes october 5. Capital gain is taxed at half (50%) Settlement date: trade day + 3 business days (t + 3) Deemed deposition: sold at fair market value. Capital loss: only to offset your capital gain, allowable/net capital loss. Amended return: if you have no capital gain, but capital loss, carry back 3 years, have to file for it. Listed personal property lpp (page 103: example: collectibles, paintings, only offset by the capital loss in this category, carry back 3 years. Personal used property (pup: no matter how much they cost, minimum value = ,000, proceed and acb. Intention to flip = business income: ex. Business investment loss: that is equity/debt from a small company, if you incurred a loss, it qualifies for a small business corporation, small business corporation: Not controlled by foreign or public company. 90% of more of assets is to engage in the active business.