BUS 251 Lecture 3: Chapter 3 notes

24 Feb 2016

School

Department

Course

Professor

Document Summary

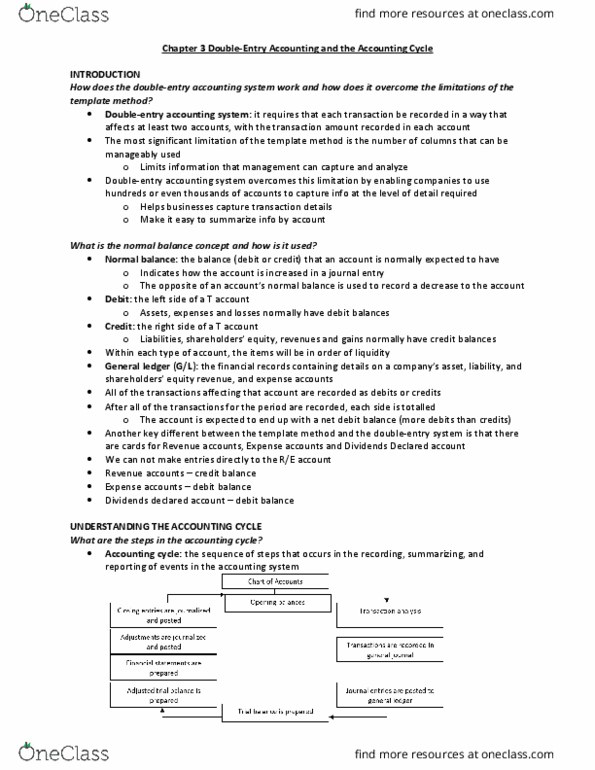

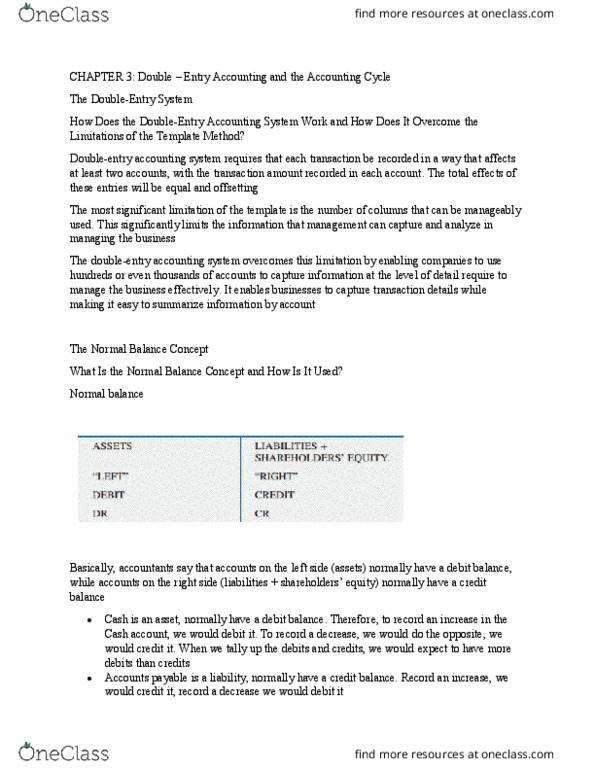

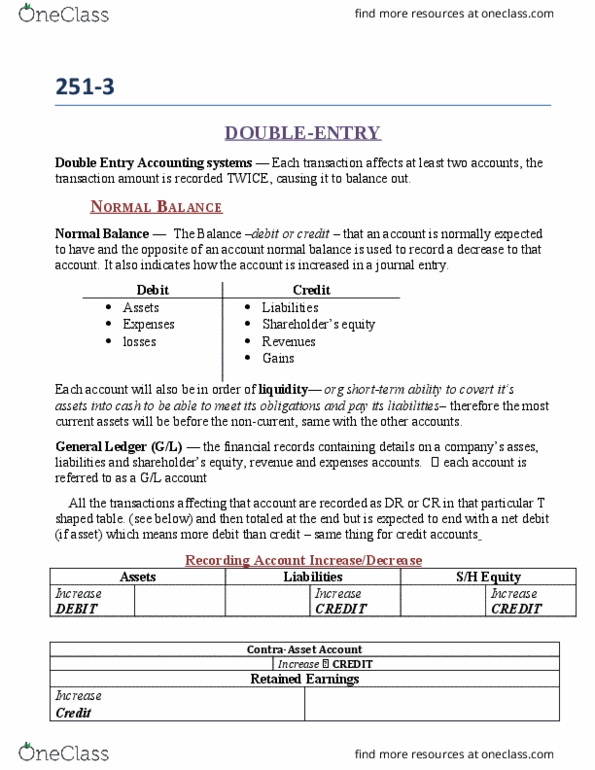

Double-entry accounting system: requires that each transaction be recorded in a way that affects at least two accounts. This method can overcome the limitation of using the template method by enabling companies to use hundreds or even thousands of accounts to capture information at the level of detail required to manage the business effectively. Normal balance: the balance (debit or credit) that an account is normally expected to have. Assets, expenses and losses normally have debit balances (left side of t account) Liabilities, shareholders" equity, revenues and gains normally have credit balances (right side of t account) Each type of accounts is listed in order of liquidity (ability to convert its assets into cash to be able to meet its obligations and pay its liabilities) Another key difference between the template method and the double-entry accounting system is that there are revenue, expense and dividends declared accounts.