BUS 251 Lecture Notes - Lecture 6: Petty Cash, Bank Reconciliation, Internal Control

14 May 2016

School

Department

Course

Professor

Document Summary

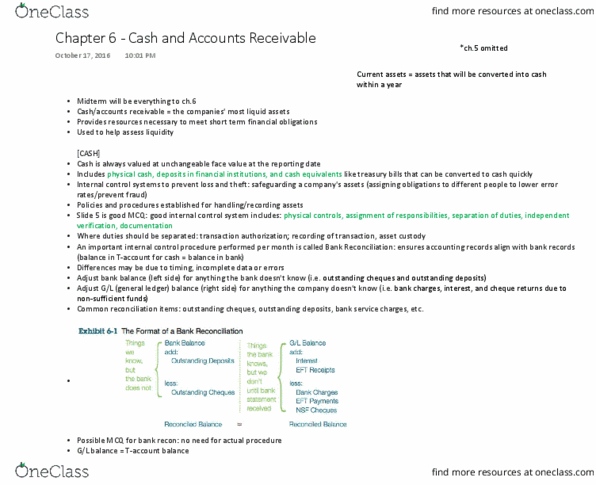

Includes cash equivalents: like treasury bills: measured in canadian dollars. Internal control systems: regulations to protect cash: safeguarding a company"s assets: a. i. Internal controls to prevent loss of theft a. ii. Policies and procedures established for handling and recording assets: a good internal control system includes b. i. The person who reconciles the bank account should not be the same person who is responsible for mainting the bank account in the accounting records segregation of duties. b. iv. Bank reconciliation: investigates ledger balance vs bank balance and finds everything that hasn"t yet been posted at the bank, such as fees, cheques, deposits, payments, bank errors. b. iv. 1. a. Ensures that the accounting records agree with the bank records b. iv. 1. b. Differences may be due to timing, incomplete data, or errors b. iv. 1. c. Some cash should be left on hand to pay minor expenses, petty cash : accounts receivable, bad debt: an amount should be set aside for this, a/r valuation: b. i.