BUS 320 Lecture Notes - Lecture 22: Cash Flow, Retained Earnings, Accrued Interest

29 Nov 2017

School

Department

Course

Professor

Document Summary

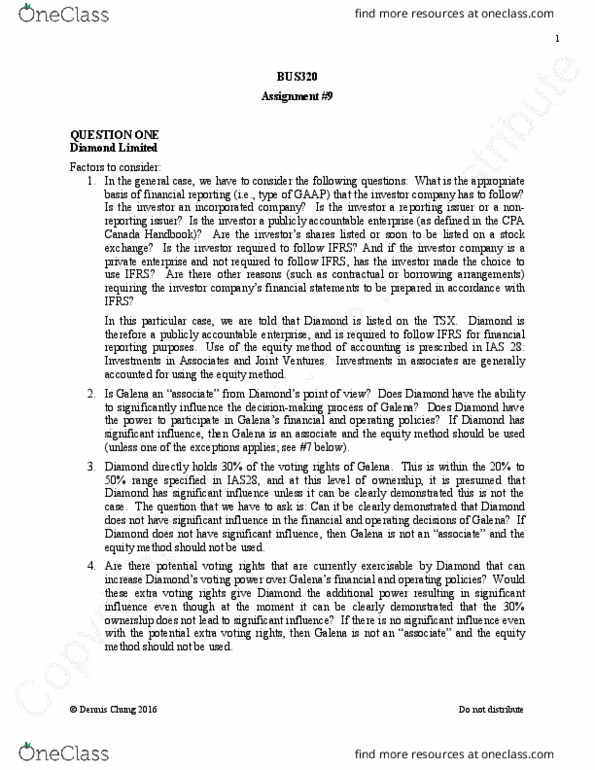

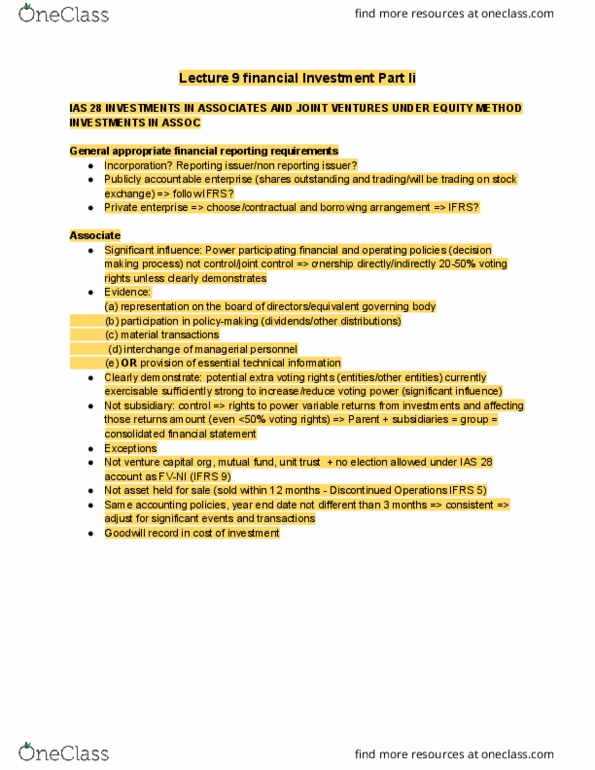

Possible scenarios and conditions that have to be satisfied to justify and support the following accounting treatment: (i) flamingo accounting for its investment in the nighthawk bonds as a financial asset measured at amortised cost . We also need to make sure that the selling of financial assets is not an integral part of. Flamingo"s business model in making all its investments such as the investment in the. This is a factor to consider because if there is significant influence or control, then ifrs9 does not apply (with an exception which we will cover in lecture. 9); for example, ias28 applies if there is significant influence, and ifrs3 and ifrs10 apply if there is control (and we will cover ias28, ifrs3 and ifrs10 in lecture 9 too). If one (or both) of these two conditions for the use of the amortised cost model is not met, then.