BUS 320 Lecture Notes - Lecture 7: Deferred Income, Cash Flow, Interest Expense

16 Sep 2016

School

Department

Course

Professor

Document Summary

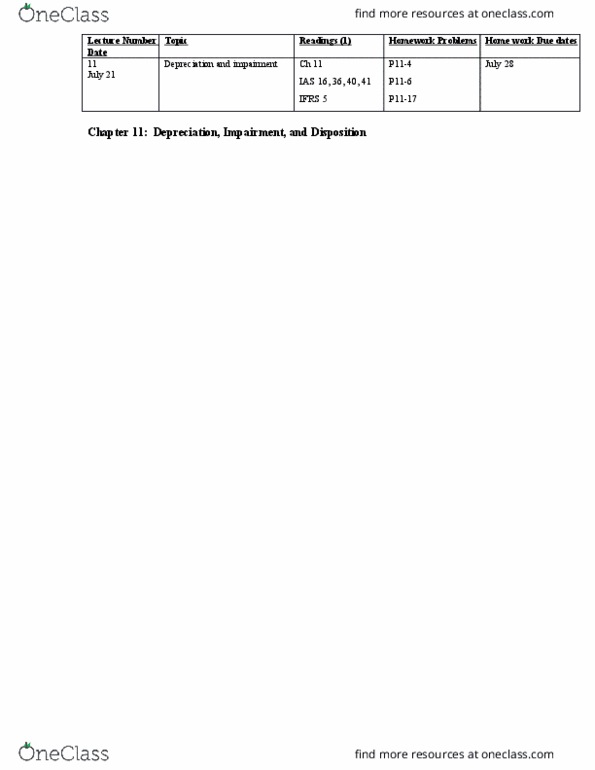

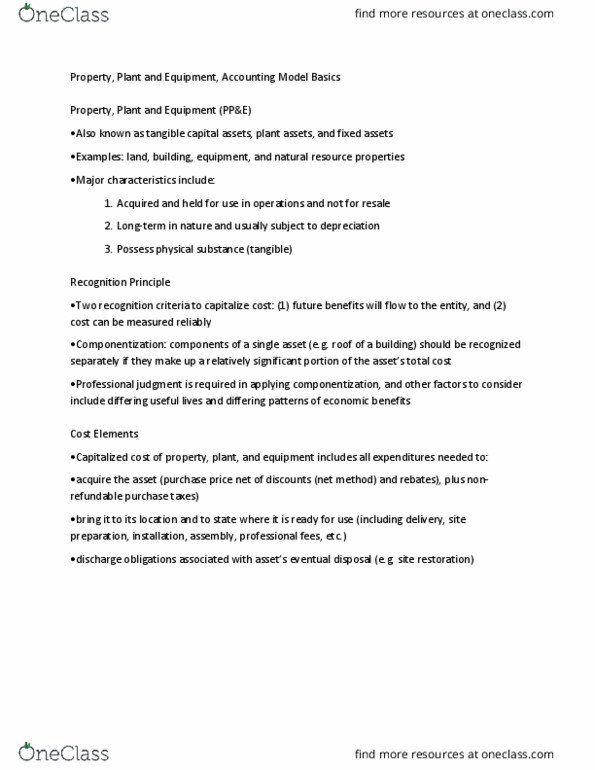

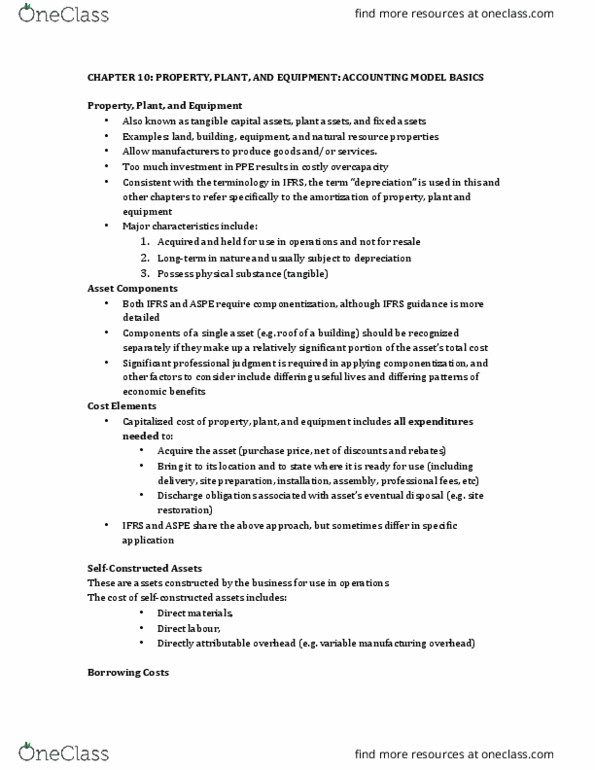

July 21, 2016: property, plant, and equipment (tangible capital assets) The assets that have the following characteristics: tangible (possess physical substances, acquired and held for use in operations and not for resale, long term in nature and usually subject to depreciation. Components of a single asset should be recognized separately if they make up a relatively significant portion of the asset"s total cost. The significant professional judgment is required in applying componentization, and other factors to consider include differing useful lives and differing patterns of economic benefits. Note: ifrs and aspe require componentization, although ifrs guidance is more detailed. The assets that are constructed by the business for use in operations are the self- constructed assets. The costs of these assets are: direct material, direct labor, directly attributable overhead (e. g. variable manufacturing overhead) Note: no fixed overhead is usually charged to the pp&e asset.