BUS 426 Lecture Notes - Lecture 3: Audit Risk, Internal Control, Financial Statement

19 Sep 2012

School

Department

Course

Professor

Document Summary

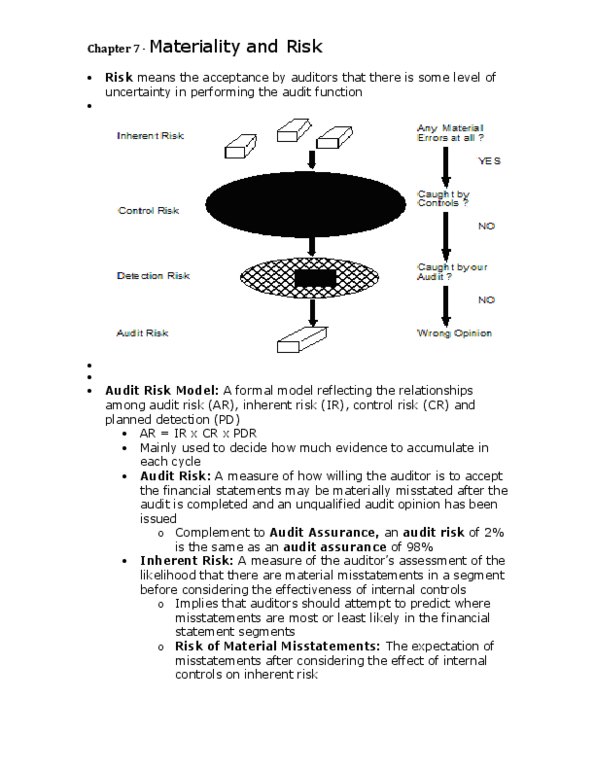

Tactical phase = performance of audit tests. Audit procedures are designed to satisfy audit objectives in order to reduce the probability of misstatement. Also a risk when the auditor states that the statements are unfairly statement damage reputation. Auditors can"t test for everything, so they do take an amount of risk. Usually for large firms, audit risk is lower (in comparison to small firms), this is because more users use the financial statements for large firms. Components of an audit risk: inherent risk: unavoidable risks, control risk: internal controls, catches some misstatements, detection risk: auditor controls, catches more misstatements. Audit risk = ir x cr x dr. Multiplicative means they are independent of each other. Ar, ir, cr are all assessment inputs, and dr is the output, influences the extent of testing. So rewritten as: dr = ar / (ir x cr: if ar goes up, so does the dr and vise-versa.