BUS 426 Lecture Notes - Lecture 9: Contingent Liability, Analytical Review, Financial Statement

19 Sep 2012

School

Department

Course

Professor

Document Summary

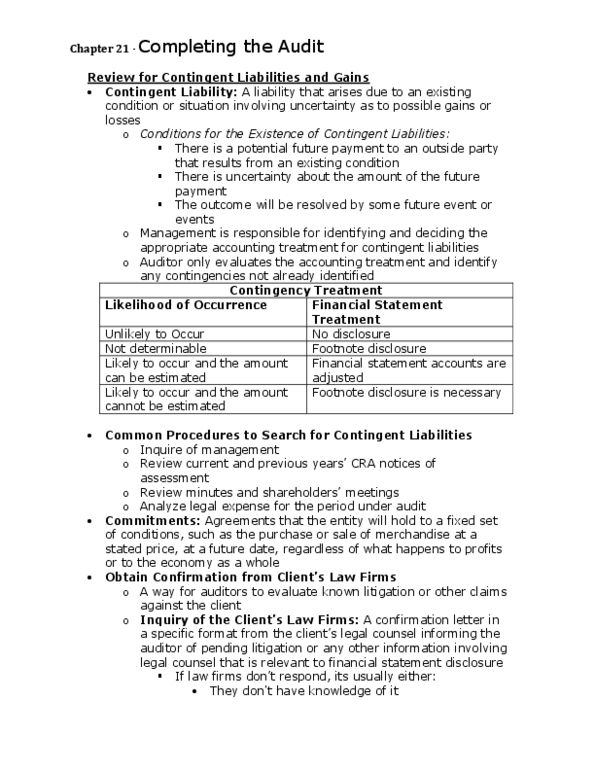

Cls are existing conditions or situation that will be resolved at some future time eg. lawsuit. How to search for cl: enquire of management, review minutes of shareholders. Board of director meetings: read contracts, agreements + related correspondence, legal inquiry most important. Legal inquiry = legal confirmation: confirmation letter in a specific format (fig. Requesting information about pending litigation or other relevant information with respect to legal claims. 2 categories of claims: outstanding or asserted claims. Client has been notified of the suit or the suit has already been filed: possible or unasserted claims. Client is aware of a situation that could lead to. Legal expenses claims: analysis to get indication of contingent liabilities, identify law firms where confirmations are required, identify events that need to be confirmed by law firms. Evaluate known contingent liabilities: once the cl has been identified and documented, then management"s disclosure of the cl needs to be evaluated, based on the likelihood of event.