BUS 315 Lecture 6: Solutions_Ch_6_doc

19 Jun 2016

School

Department

Course

Professor

Document Summary

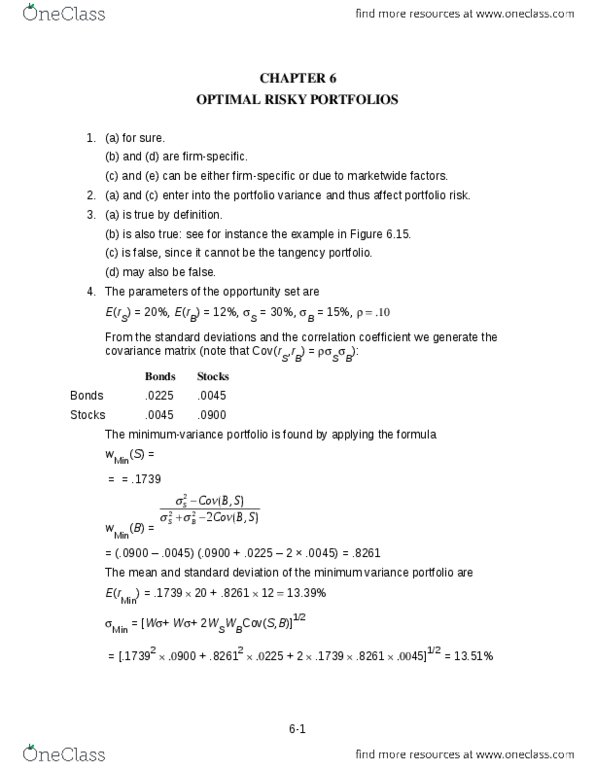

1. (a) for sure. (b) and (d) are firm-specific. (c) and (e) can be either firm-specific or due to marketwide factors. 2. (a) and (c) enter into the portfolio variance and thus affect portfolio risk. 3. (a) is true by definition. (b) is also true: see for instance the example in figure 6. 15. (c) is false, since it cannot be the tangency portfolio. (d) may also be false. E(rs) = 20%, e(rb) = 12%, s = 30%, b = 15%, . From the standard deviations and the correlation coefficient we generate the covariance matrix (note that cov(rs,rb) = s b): The minimum-variance portfolio is found by applying the formula w (s) = . 0900 + . 0225 2 . 0045 w (b) = The mean and standard deviation of the minimum variance portfolio are. ) = . 1739 20 + . 8261 12 13. 39% = [. 17392 900 + . 82612 225 + 2 . 1739 . 8261 45]1/2 = 13. 51%