BUS 321 Lecture Notes - Lecture 5: Dividend, Capital Structure, Treasury Stock

3 Feb 2018

School

Department

Course

Professor

Document Summary

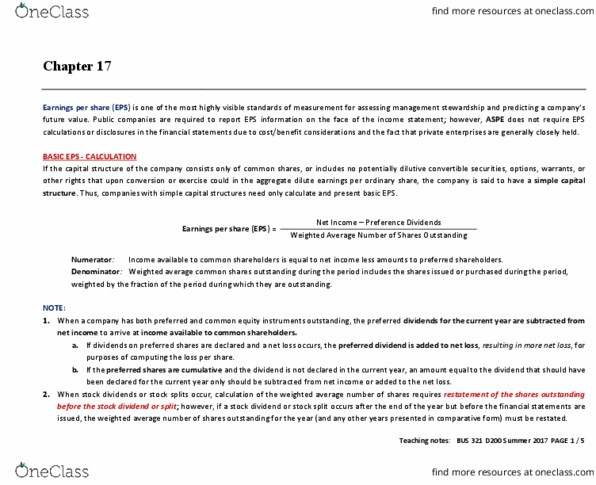

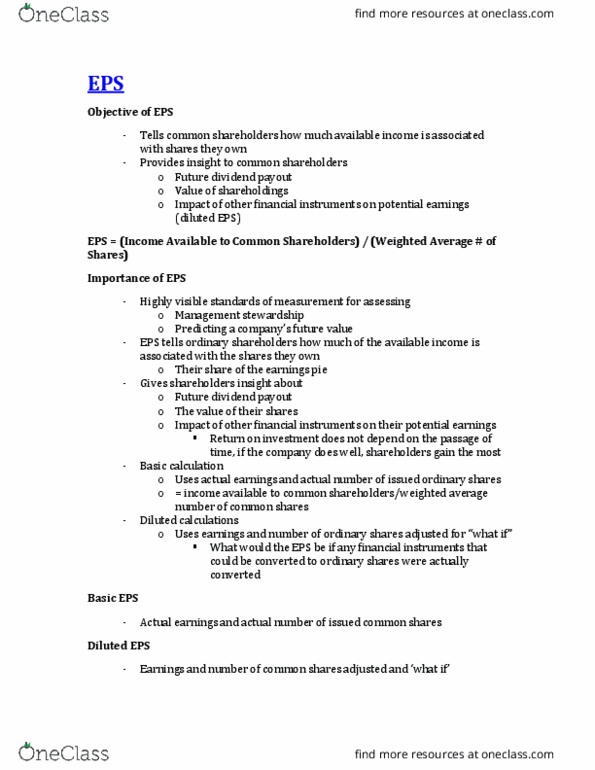

Eps: net earning attribute to each cs = ni - preferred dividends/ wa # cs outstanding. Compare perf of firms of varying sizes. Report for each income component: access future dividend payout, value shareholdings, Indicate amount available ni associated with shares own ( profit share/earnings pie) impact of financial instruments + specific income from continued operation + gain/loss from irregular item on eps. Stewardship management, predict future value => carefully analysis dilutive impact of financial instruments = difficult, complex. Ifrs cpa handbook, section 3500. 60 requires in is => except non public, private corp. Both basic and diluted if complex capital structure => dilute report at least 1 period = report for all periods present. Prior period: restated if stock dividends, stock splits. Current period: restated if restatement of prior period operations (error correction) Simple => complex capital structure: determine options, warrants, convertible debt and. Ps outstanding each period => issuance + redemption change capital structure and reflected in eps.