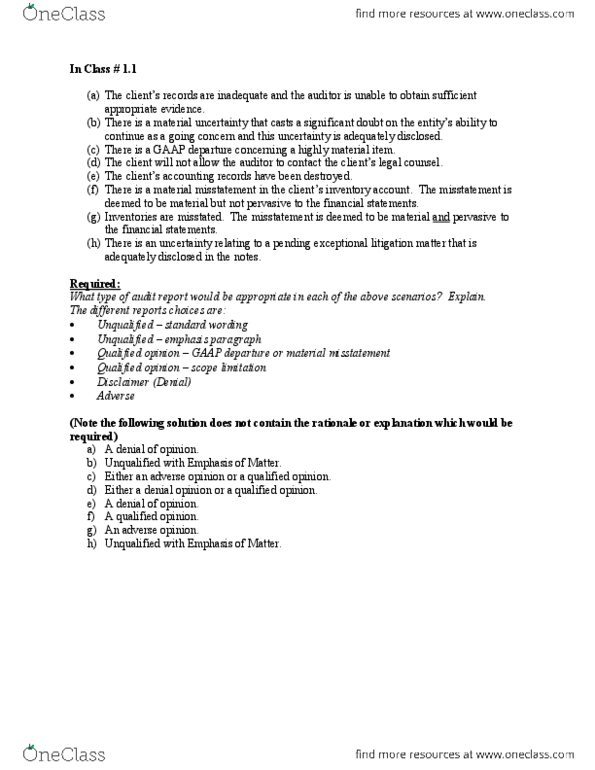

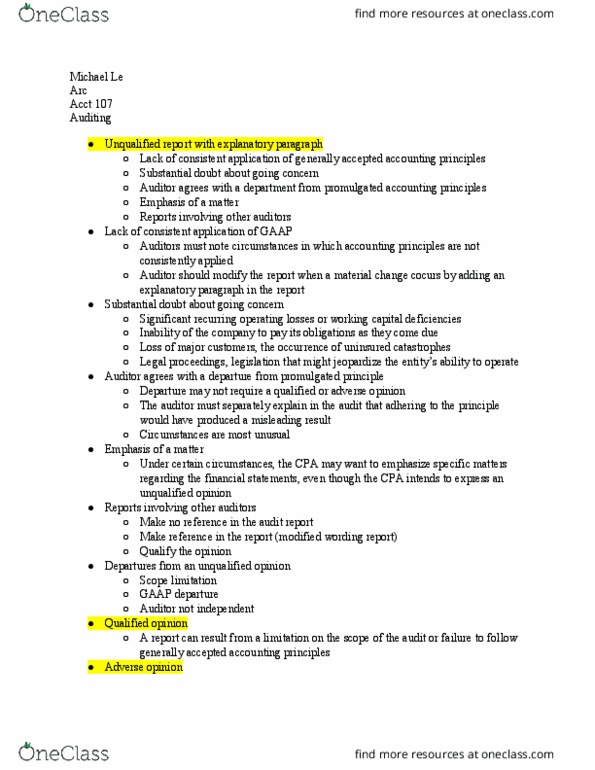

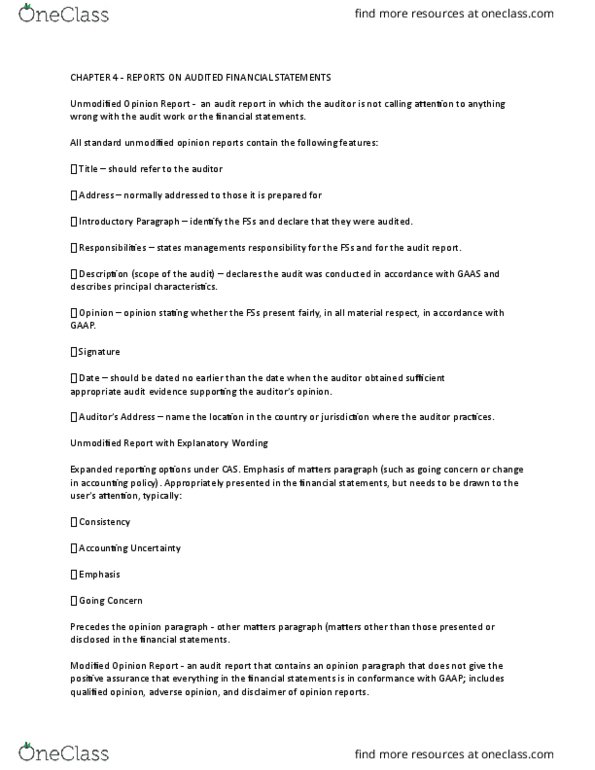

Chapter 15

1. Consider the following statements:

I. For the last several years, both the FinancialAccounting Standards Board (FASB) and the

International Auditing and Assurance Standards Board (IAASB)have been considering possible

changes to the standard unqualified audit report.

II. The audit report is modified to five paragraphs as a resultof another audit firm performing part of

the financial statement audit (Refer to Shared Reporttopic).

a. I is true; II is true

b. I is true; II is false

c. I is false; II is true

d. I is false; II is false

2. Consider the following statements:

I. Inconsistent application of accounting principles is a GAAPviolation and would result in a

qualified or adverse audit opinion.

II. For a change in accounting principles thatmanagement does justify to the auditor, the

auditor will likely choose between a qualified or an adverseopinion.

a. I is true; II is true

b. I is true; II is false

c. I is false; II is true

d. I is false; II is false

3. Consider the following statements:

I. The failure of a client to include a Statement of Cash Flowswill result in the issuance of a

disclaimer of opinion by the auditor.

II. The auditor will issue an unqualified opinionon Internal Controls over Financial Reporting (ICFR)

if the auditor has identified only one material weakness inICFR.

a. I is true; II is true

b. I is true; II is false

c. I is false; II is true

d. I is false; II is false

4. In which of the following instances would an auditor mostlikely issue a standard unqualified opinion

WITH an explanatory paragraph?

a. Management disclosures are missing or inadequate.

b. There is substantial doubt about the entityâs ability tocontinue as a going-concern.

c. There is a significant limitation on the scope of theengagement.

d. There is an immaterial deviation from GAAP related tocapitalizing repairs.

5. Which one of the following is an example of the contents ofan opinion paragraph found in an audit

report?

a. âWe have audited â¦â

b. âNothing came to our attentionâ¦â

c. âThe financial statements referred to above present fairlyâ¦â

d. âAn audit includes examining, on a test basis â¦â

6. A client company has a history of negative cash flow trendsand continuing losses. What would this

seem to involve?

a. GAAP problem

b. Going concern.

c. Lack of consistency.

d. Lack of independence.

7. An audit of the Flagler Company, a diamond mining company,brings to light the fact that its

equipment has been marked up to the ownersâ expectation ofmarket values. Such a situation will

most likely result in which type of report?

a. Disclaimer.

b. Review.

c. Adverse.

d. Unqualified, with explanatory paragraph.

8. In which of the following instances would an auditor issue adisclaimer of opinion?

a. Lack of consistency.

b. GAAP problem.

c. There is a significant limitation on the scope of theengagement.

d. The principle auditor decides to make reference to anotherauditor who has issued an unqualified

audit report.

9. When might an auditor modify the introductory paragraph andreplace the scope paragraph with an

explanatory paragraph? The ANSWER is A.

a. When a pervasive scope limitation exists.

b. When there is substantial doubt about going-concern.

c. When the auditor lacks independence.

d. When there is an emphasis of a matter.