ACCTG322 Lecture Notes - Lecture 6: Earnings Before Interest And Taxes, Contribution Margin, Fixed Cost

17 Apr 2015

School

Department

Course

Professor

Document Summary

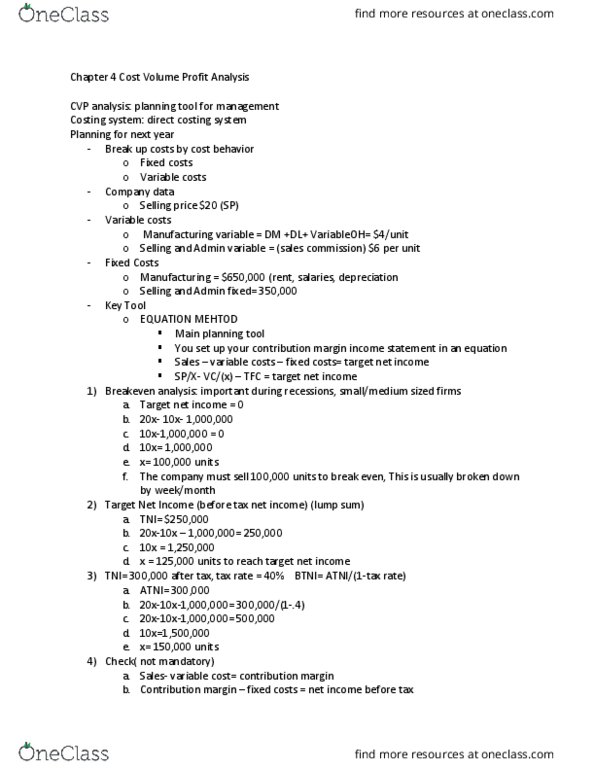

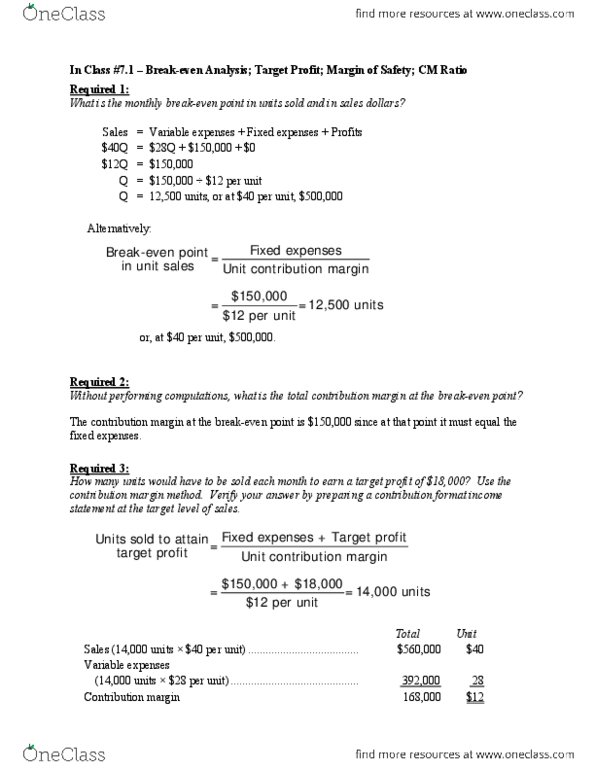

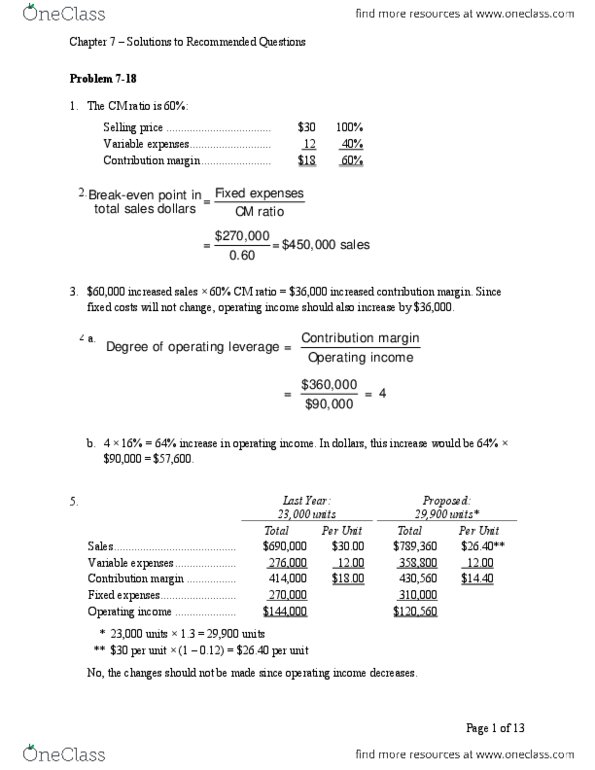

Objectives: contribution margin and contribution ratio, break-even analysis, break-even point, cvp graph, target operating profit, margin of safety, cost structure and profit stability, operating leverage, sales mix. Cost-volume-profit analysis: the effects of changes of costs and volume on a company"s profits, a critical factor in management decisions, considers the interrelationships among the five components of cvp analysis. Important in profit planning: volume or level of activity, unit selling prices, variable cost per unit, total cost per unit, sales mix. All costs are fixed or variable (or can be broken out this way). All revenue and variable costs are constant per unit. Constant contribution margin (unit sales price- unit variable cost) Basic formulas: total revenue = selling price * number of units sold, total costs = fixed costs + (variable costs * # of units sold, contribution margin (cm) = sales variable costs.