ECON101 Lecture Notes - Lecture 22: Perfect Competition, Marginal Revenue, Profit Maximization

24 Oct 2018

School

Department

Course

Professor

ECON101 verified notes

22/41View all

Document Summary

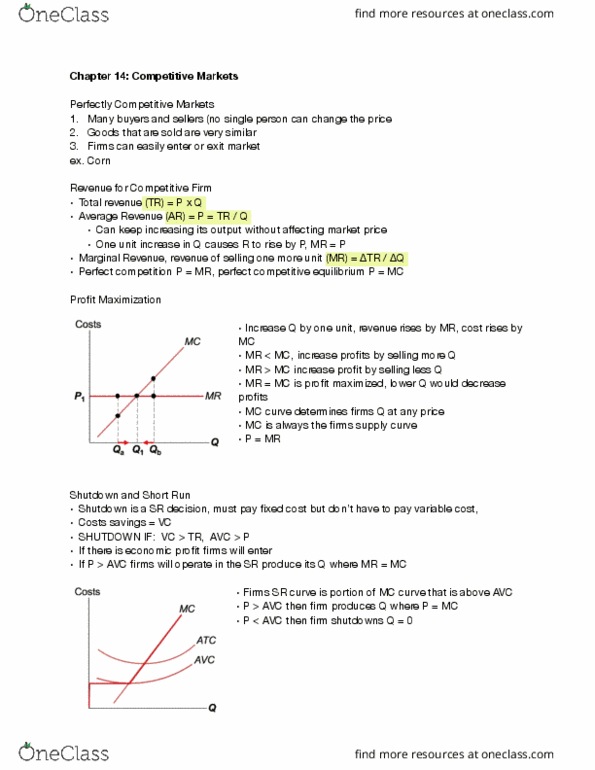

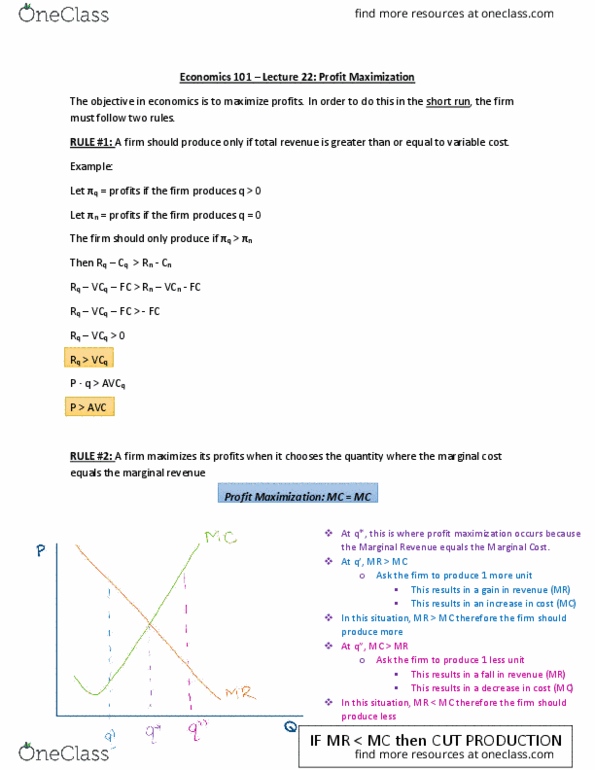

The objective in economics is to maximize profits. In order to do this in the short run, the firm must follow two rules. Rule #1: a firm should produce only if total revenue is greater than or equal to variable cost. Let q = profits if the firm produces q > 0. Let n = profits if the firm produces q = 0. The firm should only produce if q > n. Then rq cq > rn - cn. Rq vcq fc > rn vcn - fc. Rq vcq fc > - fc. Rule #2: a firm maximizes its profits when it chooses the quantity where the marginal cost equals the marginal revenue. At q*, this is where profit maximization occurs because the marginal revenue equals the marginal cost. At q", mr > mc: ask the firm to produce 1 more unit, this results in a gain in revenue (mr, this results in an increase in cost (mc)