ACCT 301 Lecture Notes - Fixed Cost, Variable Cost, Specific Volume

Document Summary

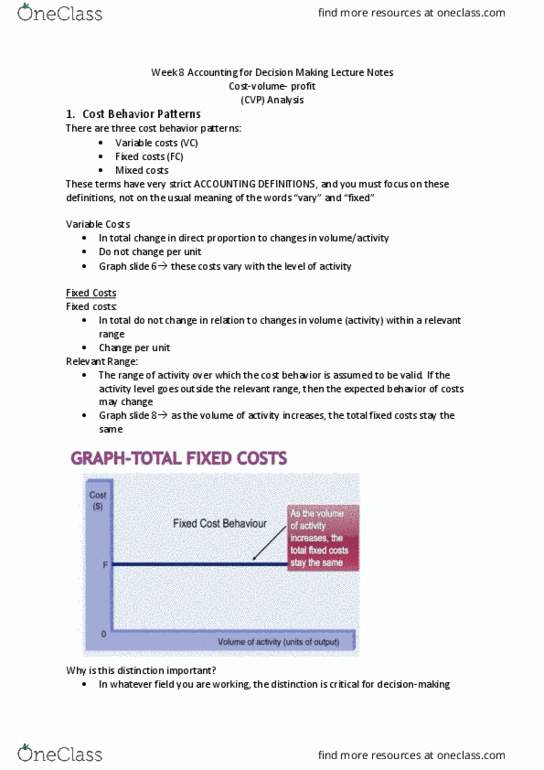

The knowledge of cost behavior is essential for the tasks of budgeting, decision making and control accounting, whose importance was established in the previous article. Cost behavior is the way in which costs are affected by changes in the volume of output. In other words, this article will attempt to describe the behavior of various costs with the volume of output. A cost behavior pattern could be established for certain costs that behave" in a. Predefined" or usual" way, which we may illustrate graphically. In the course of this article we will discuss the cost behavior of the following items: fixed costs, step costs, variable costs, semi-variable costs, total costs and unit costs. Fixed costs these costs are not generally related to the volume of output or to the level of activity within a firm, although they do increase with time.