AFM101 Lecture Notes - Accrual, Net Income, Income Statement

9 Dec 2012

School

Department

Course

Professor

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

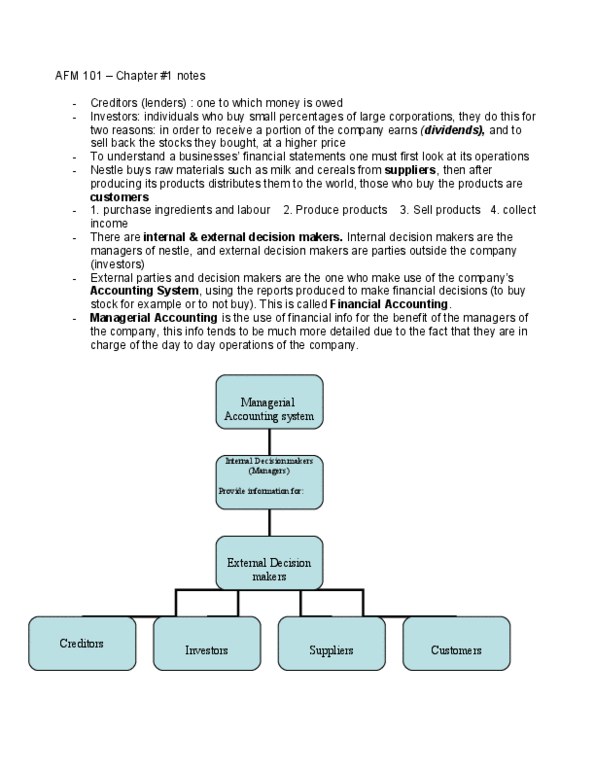

Doing accounting for user"s outside of the company(shareholders, potential shareholders) Very important, helps decide where to allocate money, whether to buy shares, where to buy shares. (e. g. pension plans deciding where to invest money, analyse financial statements to decide where they"re going to invest money, be able to understand financial statements, whether company is a winner or a loser) Understand annual report, broad perspective, understand company"s financial condition. Focus on course: standards of canadian profit-oriented organizations. Goal is not to make profit (e. g. hospitals, charities, colleges and universities) Influenced by politics, evolve over time, accounting standards different in every country. In canada, three sources: international financial reporting standards (ifrs), used in 120 countries around the world created by iasb (international accounting standards board) In us, financial accounting standards board (fasb) us generally. Public companies shares traded on the stock exchange (e. g.