AFM491 Lecture Notes - Lecture 2: Deferral, Equity Method, Accrual

16 Mar 2017

School

Department

Course

Professor

Document Summary

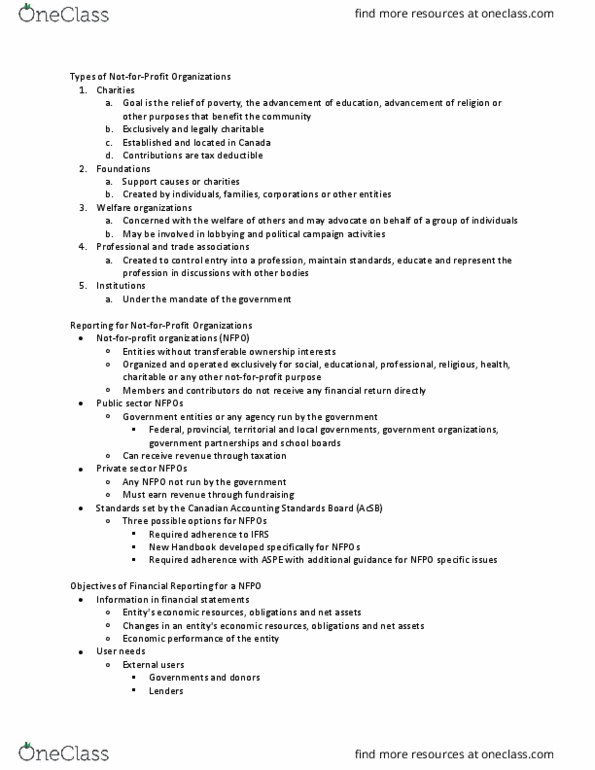

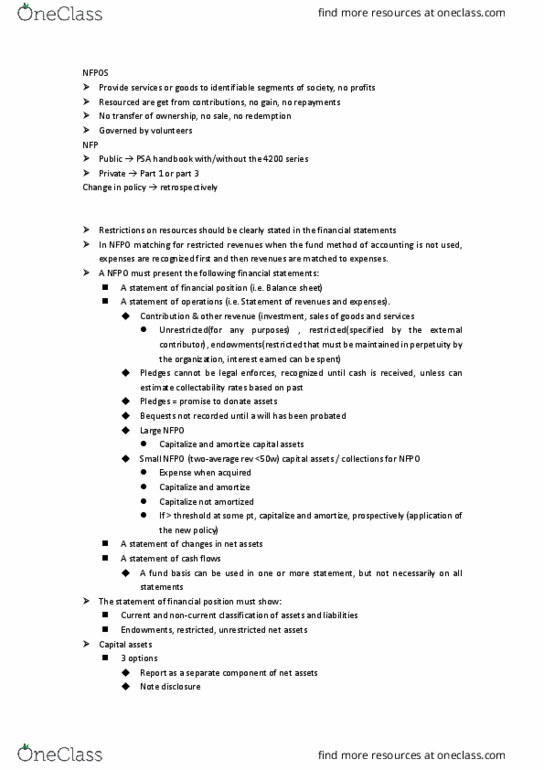

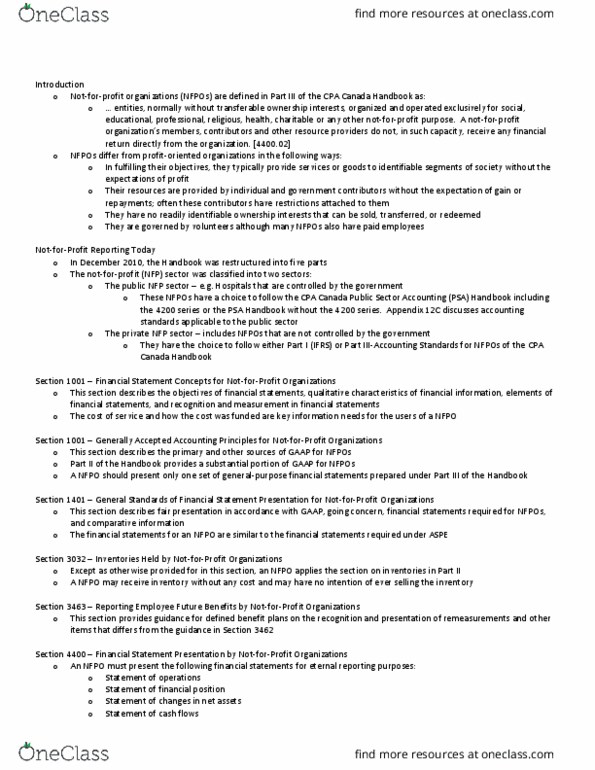

Chapter 12 accounting for not-for-profit and public sector organizations. Organizations who provide services and products on a non-profit basis: government sector federal, provincial, local, not for profit sector charities, hospitals, universities, professional and fraternal organizations, and community clubs. Charity: nfpo that must devote its resources to charitable activities, ca(cid:374)"t use i(cid:374)(cid:272)o(cid:373)e for perso(cid:374)al (cid:271)e(cid:374)efit of its (cid:373)e(cid:373)(cid:271)ers or go(cid:448)er(cid:374)i(cid:374)g offi(cid:272)ials. I(cid:374)for(cid:373)atio(cid:374) of (cid:373)a(cid:374)age(cid:373)e(cid:374)t"s dis(cid:272)harge of ste(cid:449)ardship has management appropriately utilized its resources according to the wishes/restrictions given by those providing the resources. Internally restricted and other externally restricted net assets: unrestricted net assets. ** net assets invested in capital assets used to have to be shown as a separate component of net assets but now it can be shown separately, or just disclosed in notes, or neither. Retrospective accounting is forbidden in the following cases: de-recognition of financial assets and financial liabilities, hedge accounting, estimates, non-controlling interests. Inventory received at no-cost with no intention of selling at fv: