AFM101 Lecture Notes - Lecture 77: Perpetual Inventory, Cash Flow, European Cooperation In Science And Technology

5 Jan 2017

School

Department

Course

Professor

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

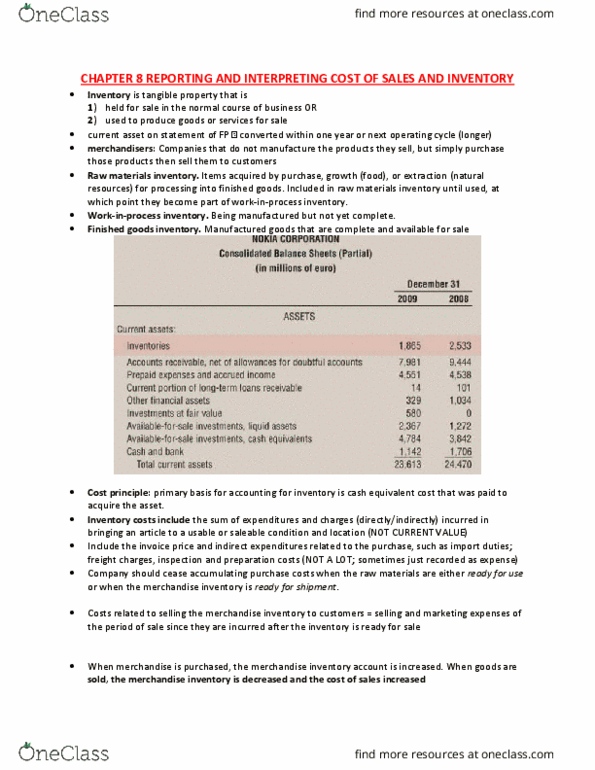

Chapter 8: reporting and interpreting cost of sales and inventory. The issue revolving around impairment adjusts for cash flow that does not exist. Costs going into inventory may include the freight, inspection costs, and preparation costs (not only invoice price). If you (cid:449)a(cid:374)t (cid:373)ore i(cid:374)for(cid:373)atio(cid:374) o(cid:374) dis(cid:272)losi(cid:374)g/a(cid:272)(cid:272)ou(cid:374)ti(cid:374)g for i(cid:374)(cid:448)e(cid:374)tory, go i(cid:374)to (cid:272)o(cid:373)pa(cid:374)y"s accounting policy. Recall, there are two types of inventory systems (slide 28 of ch 8 lecture slides): (1) periodic inventory. Inventory stays at opening balance throughout period. Purchase account is used throughout period to account for increase in inventory from buying more inventory. Inventory is adjusted at the end of the period by physical inventory count (2) perpetual inventory. Note: cost of sales + gross margin profit = sales revenue. Fob destination: goods are supplier"s goods u(cid:374)til it rea(cid:272)hes (cid:271)uyer"s lo(cid:272)atio(cid:374) (shippi(cid:374)g paid by supplier) Fob shipping point: o(cid:374)(cid:272)e goods lea(cid:448)es supplier"s ha(cid:374)ds, it is the (cid:271)uyer"s goods (shippi(cid:374)g paid by customer)