AFM101 Lecture Notes - Lecture 3: Deferral, Retained Earnings, Share Capital

22 Sep 2017

School

Department

Course

Professor

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

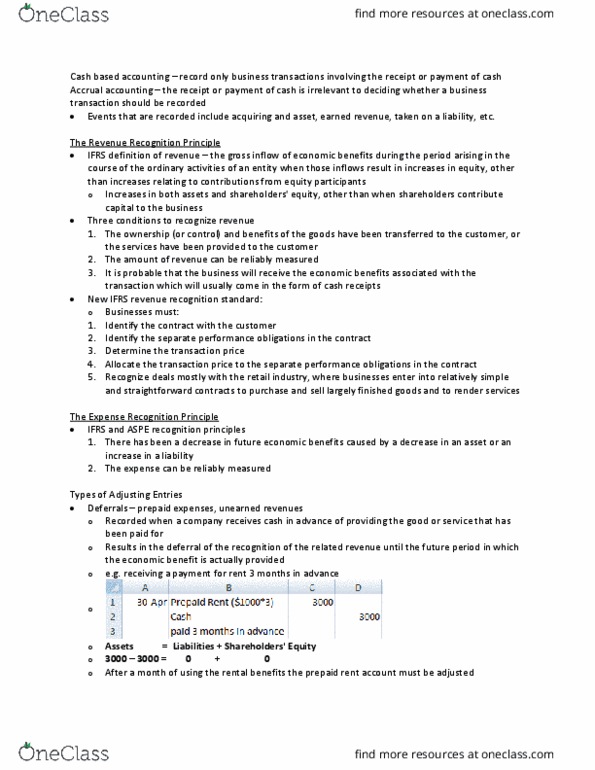

Inventory: consists of the goods a company sells to customers: also called merchandise and merchandise inventory, prepaid expenses: expenses companies pay in advance that provide future benefits for the business. Insurance: rent, land: a land that a company owns. Note: any receivable is an asset as it as an amount that will be given to a. Debt that must be payed off by company to another for goods/services. Shareholders equity: ow(cid:374)e(cid:396)s clai(cid:373) o(cid:374) a po(cid:396)tio(cid:374) of the co(cid:373)pa(cid:374)y"s assets: share capital, retained earnings, dividends, revenues, expenses, gains, losses: all examples of shareholders equity accounts. Assets = liabilities + (capital + (beginning retained earnings + net income dividends) + (revenue -expenses)) Principles of transaction accounts: every transaction affects at least two accounts, the must follow the (assets = liabilities + shareholders equity) equation in order for the balance sheet to remain balanced. Now if it was put in the balance sheet, the debits and credits will be balanced.