AFM101 Lecture Notes - Lecture 16: Book Value, Product Return, Intangible Asset

1 Nov 2018

School

Department

Course

Professor

AFM101 verified notes

16/21View all

Document Summary

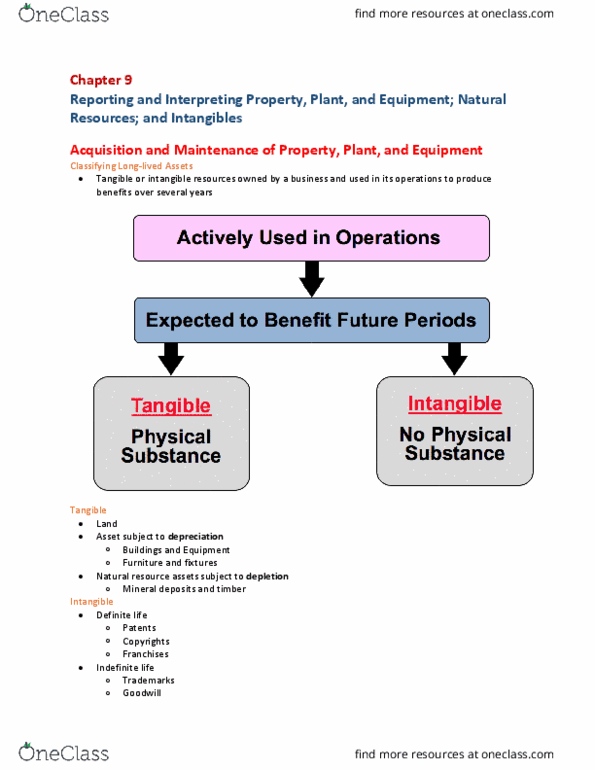

Companies purchase plant assets whenever they need them, not just at the beginning of the year. Thus, companies must compute depreciation for partial years. Partial depreciation = (cid:1866)(cid:1866)(cid:1873) (cid:1868)(cid:1872)(cid:1867)(cid:1866) (cid:3014)(cid:3042)(cid:3041)(cid:3047) (cid:3046) (cid:3033)(cid:3045)(cid:3042)(cid:3040) (cid:3031)(cid:3047)(cid:3032) (cid:3042)(cid:3033) (cid:3043)(cid:3048)(cid:3045)(cid:3030) (cid:3046)(cid:3032) (cid:3047)(cid:3042) (cid:3052)(cid:3032)(cid:3045) (cid:3032)(cid:3041)(cid:3031) (cid:2869)(cid:2870) After an asset is in use, managers may change its useful life on the basis of. This is called a change in accounting estimate. (cid:3045)(cid:3045)(cid:3052)(cid:3041)(cid:3034) (cid:3040)(cid:3042)(cid:3048)(cid:3041)(cid:3047) (cid:3047) (cid:3031)(cid:3047)(cid:3032) (cid:3042)(cid:3033) (cid:3030) (cid:3041)(cid:3034)(cid:3032) (cid:3032)(cid:3046)(cid:3031)(cid:3048)(cid:3039) (cid:3049)(cid:3039)(cid:3048)(cid:3032) (cid:3047) (cid:3031)(cid:3047)(cid:3032) (cid:3042)(cid:3033) (cid:3030) (cid:3041)(cid:3034)(cid:3032) (cid:3032)(cid:3040)(cid:3041)(cid:3041)(cid:3034) (cid:3048)(cid:3046)(cid:3032)(cid:3033)(cid:3048)(cid:3039) (cid:3039)(cid:3033)(cid:3032) (cid:3047) (cid:3031)(cid:3047)(cid:3032) (cid:3042)(cid:3033) (cid:3030) (cid:3041)(cid:3034)(cid:3032) A fully depreciated asset is an asset that has reached the end of its estimated useful life. The carrying value of a fully depreciated asset is zero. If the company continues to use a fully depreciated asset, it will not recognize any more depreciation expense for the asset but: Both the asset account and its accumulated depreciation account remains in the ledger with no additional depreciation entries.