AFM131 Lecture : )

16 Oct 2011

School

Department

Course

Professor

22

AFM131 Full Course Notes

Verified Note

22 documents

Document Summary

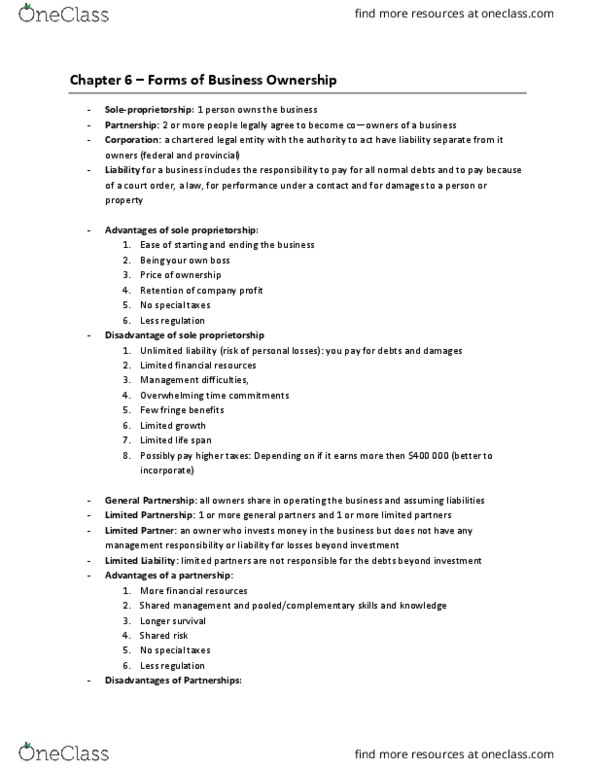

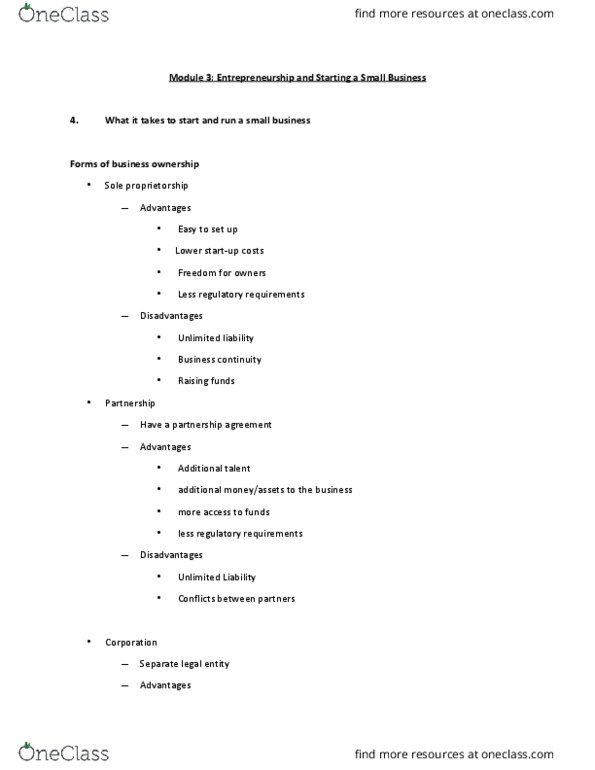

Three forms of business ownership: sole proprietorship: one person owning and operating a business, without forming a corporation. Business owner + business = single entity: partnership: a legal form of business with two or more parties, corporation: a legal entity with authority to act and have liability separate from its owners. Liability for a business includes: responsibility to pay all normal debts and to pay: because of court order, because of a law, for performance under a contract, for damages to a person or property. All you have to do to start is to buy or lease needed equipment, put up announcements to say you are in business. One of the most common reasons for starting a sole proprietorship. They deserve all credit for taking risks and providing needed products. You don"t need to share money with anyone else except government/taxes. Because profit is considered yours from the get go, it is only taxed once, as your personal income.