AFM351 Lecture Notes - Lecture 10: Professional Code Of Quebec, Ethical Decision

28 Jun 2018

School

Department

Course

Professor

Who to speak first?

○

Bryan decides to first talk to his university classmates and learned that many firms are

aware of this practice and want to stamp it out because it reduces the ability of junior

employees to express themselves during engagements

○

Next, he talks confidentially to his provincial institute's peer support program and gains

information and a sense of support for his intended strategy to raise this issue with Karen

first

○

Armed with information, Bryan writes out an opening statement that clearly frames his

conversation with Karen as an opportunity for learning and moving towards best audit

practices

○

Often difficult to turn the decision into action○

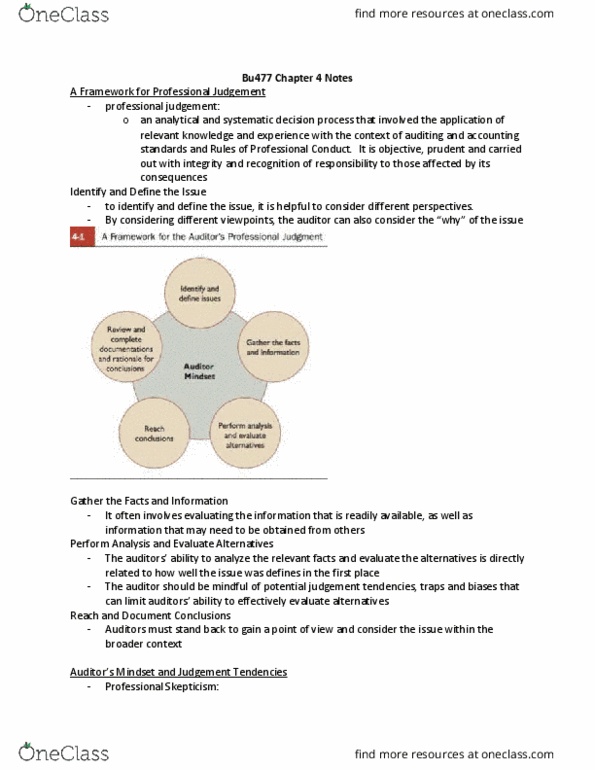

Ethical decision making process- a methodological approach to resolving an ethical dilemma•

Decision makers are susceptible to judgement traps referred to as ethical blind spots -

unconscious judgement tendencies that can hinder the ethical decision making process or cause

the decision maker to fail to recognize the ethical dimension of a choice

•

Ethical blind spots

Both the professional judgement and ethical reasoning frameworks highlight that auditors'

decisions are made with consideration of rules of professional conduct

•

It serves members by setting standards the members must meet and providing a benchmark

against which to measure member's actions

•

The professional code of conduct in Canada is both principles based and compliance based•

Critics of a principles-based code highlight that principles are difficult to enforce because there are

no minimum standards of behaviour

•

Disadvantage is the tendency of some practitioners to define the rules as maximum rather

than minimum standards

○

Second disadvantage is that some practitioners may view the code as the law and conclude

that if some action is not prohibited, it must be ethical

○

The advantage of this compliance-based approach is that the association is able to enforce

minimum behaviour and performance standards

•

Professional guidance on ethical conduct

PA must be free of an influence, interest, or relationship that impairs professional judgement or

•

Independence

AFM 351 Page 11

Document Summary

Bryan decides to first talk to his university classmates and learned that many firms are aware of this practice and want to stamp it out because it reduces the ability of junior employees to express themselves during engagements. Next, he talks confidentially to his provincial institute"s peer support program and gains information and a sense of support for his intended strategy to raise this issue with karen first. Armed with information, bryan writes out an opening statement that clearly frames his conversation with karen as an opportunity for learning and moving towards best audit practices. Ethical decision making process- a methodological approach to resolving an ethical dilemma. Often difficult to turn the decision into action. Both the professional judgement and ethical reasoning frameworks highlight that auditors" decisions are made with consideration of rules of professional conduct. It serves members by setting standards the members must meet and providing a benchmark against which to measure member"s actions.