ECON101 Lecture Notes - Lecture 6: Externality, Social Cost, Economic Surplus

6 Dec 2017

School

Department

Course

Professor

79

ECON101 Full Course Notes

Verified Note

79 documents

Document Summary

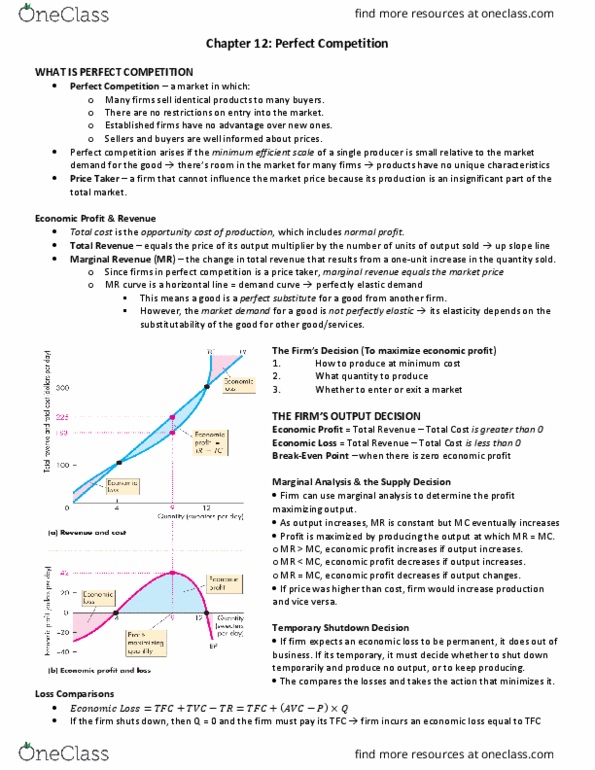

Don"t care which firm"s good they buy (no branding) Rms set their own price equal to the market price arises when: in the market (unable to affect price) In perfect competition, each firm is a price taker: a firm that cannot influence the price of a. In perfect competition, the marginal revenue is equal to the market price, the marginal revenue is constant as output increases and rms seek to maximize economic pro t. What is perfect competition: many firms sell identical products to many buyers, no restrictions to entry into the industry, established firms have no advantages over new ones, sellers and buyers are well informed about prices. No single firm can influence the price- it must take equilibrium market price. Each firm"s output (product) is a perfect substitute for the output of the other firms so the demand is perfectly elastic. Total cost is the opportunity cost of production which includes normal profit.