ECON101 Lecture Notes - Price Ceiling, Economic Equilibrium, Demand Curve

ECON101 Full Course Notes

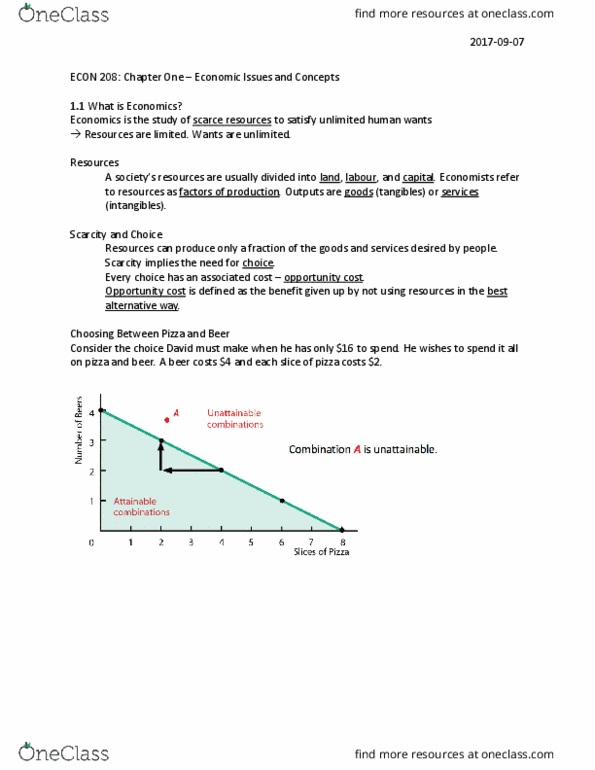

Document Summary

Get access

Related Documents

Related Questions

1) Which of the following transactions would be included in GDP?

a) The purchase of a Monet painting.

b) The purchase of paper clips.

c) The purchase of Telstra shares.

d) The purchase of a used car.

2) Economics is the study of

a) the choices everybody makes to attain their goals, given their scarce resources.

b) supply and demand.

c) how to make money in a market economy.

d) how to make money in the stock market.

3) The economy is considered to be at full employment when

a) all unemployment is voluntary.

b) all unemployment is frictional or structural.

c) there are no unemployed workers.

d) there are more unemployed workers than job vacancies

4) An example of an intermediate good would be

a) a can of cool drink sold by a super‐market.

b) a microwave used at home.

c) the bread that goes into a sandwich sold by a lunch bar.

d) the petrol purchased by consumers for their cars

5) From 2004 to 2005, the CPI for medical care increased from 260.8 to 272.8. What was the inflation rate for medical care?

a) 12 percent

b) 11.1 percent

c) 4.9 percent

d) 4.6 percent

6) A shift outwards of the nation's production possibility frontier can occur from

a) a reduction in unemployment.

b) an increase in the size of the labour force.

c) a change in the amounts of one good desired.

d) a natural disaster like a hurricane or severe earthquake

7) What assumptions about humans do economists make?

a) People are greedy and selfish.

b) None, because economics takes humans as given.

c) People are rational and respond to incentives.

d) Humans prefer to live in a society that values fairness above all else.

8) The labour force is the

a) a number of people employed minus the number of people unemployed.

b) ratio of the number of people employed by the number of people unemployed.

c) ratio of the number of people employed to the working-age population.

d) the number of people employed plus the number of people unemployed.

9) The production possibility frontier shows

a) attainable combinations of two products that may be produced with available resources.

b) the various products that can be produced now and in the future.

c) what an equitable distribution of products among citizens would be.

d) the rate of substitution between capital and labour.

10) Which of the following transactions would be included in the official calculation of GDP?

a) Bridgestone sells $2 million worth of tyres to General Motors Holden

b) You illegally download music off the Internet to put on your new iPod.

c) A new iPod.

d) A student buys a used textbook at the bookstore.

11) What are the three fundamental questions that any economy must answer?

a) What will be the prices of goods, how will these goods be produced, and who gets them?

b) What will be the prices of goods, what will be produced, and who gets them?

c) What will be produced, how will these goods be produced, and who gets them?

d) How much will be saved, what will be produced, and how can these goods be fairly distributed?

12) If the nominal interest rate is 6% and the inflation rate is 2%, then the real interest rate is

a) 3%.

b) 2%.

c) 4%.

d) 8%.

14) Suppose that a very simple economy produces three goods: movies, burgers, and bikes. Suppose the quantities produced and their corresponding prices for 2004 and 2009 are shown in the following table:

| 2004 | 2009 | |||

| Quantity | Price | Quantity | Price | |

| Movies | 20 | $6 | 30 | $7 |

| Burgers | 100 | $2 | 90 | $2.5 |

| Bikes | 3 | $1000 | 6 | $1100 |

What is real GDP in 2009, using 2004 as the base year?

a) $3690

b) $7035

c) $6360

d) $3320

15) If the production possibility frontier is graphed as a straight line, what does this mean?

a) Opportunity costs are constant as production shifts from one product to the other.

b) It is easy to efficiently produce output.

c) Nothing, there is no significance of a straight line production possibility frontier.

d) Opportunity costs are increasing as production shifts from one product to the other.

16) If you have both an economics exam and a management exam tomorrow, but find that you have time to fully study for only one of them, what are you facing?

a) A failing grade in both exams

b) A zero opportunity cost

c) A trade‐off

d) An impossible situation

17) Which of the following is a problem inherent in centrally planned economies?

a) Production managers do not satisfy consumer wants but the government's orders.

b) Too much production of low‐cost, high‐quality goods and services.

c) There are no problems, everyone, including consumers are satisfied.

d) None of these describe the problem inherent in a centrally planned economy.

18) Inflation is an increase in the

a) average hourly wage rate.

b) general price level in the economy.

c) the overall level of economic activity.

d) rate of growth of GDP.

19) Total production in the economy is measured as the

a) dollar value of all final goods and services produced in the economy.

b) the total number of services produced in the economy.

c) the total number of goods produced in the economy.

d) the total number of goods and services produced in the economy.

20) An increase in the price of dairy products produced domestically will be reflected in

a) Both the GDP deflator and the consumer price index.

b) Neither the GDP deflator nor the consumer price index.

c) The GDP deflator but not in the consumer price index.

d) The consumer price index but not in the GDP deflator.

21) The reason that opportunity cost arises is that

a) money has proven to be an inefficient means of facilitating exchange in a market.

b) sometimes there are no alternative decisions that can be made.

c) resources are limited at any point in time. d) people have unlimited wants.

21) You have an absolute advantage whenever you

a) are better educated than someone else.

b) can produce something at a lower opportunity cost than others.

c) can produce more of something than others with the same resources.

d) prefer to do one particular activity.

22) Which of the following is an example of a worker experiencing cyclical unemployment?

a) A Freightliner employee who was sacked because of a recession.

b) A worker who quits his job because he does not get along with his boss

c) A worker that changes jobs to move closer to her family.

d) An assembly line worker who loses his job because of automation.

23) A company named Home Depot sells new and used doors to contractors who build new homes. Home Depot also sells new and used doors to home‐owners. Which of the following would be counted in GDP?

a) The sale of a used door to a home‐owner

b) The sale of a used door to for construction for installation into a new home.

c) The sale of a new door to for construction for installation into a new home.

d) The sale of a new door to home‐owner.

24) If you buy shares, the dollar value is

a) not included in GDP.

b) included in GDP under consumer expenditure.

c) included in GDP as a business expense.

d) included in GDP under-investment.

25) During the 1930s, Australia and other industrialised countries experienced the Great Depression with a large number of workers and factories unemployed.Which of the following points on a production possibility frontier model would represent this experience?

a) A point on the frontier

b) A point inside the frontier

c) An increase in the opportunity cost of the substitution between capital and labour

d) A point outside the frontier

26) How is the decision about what goods and services will be produced made in a market economy?

a) The government decides on what will be produced.

b) Producing firms decide to produce only what the firms' owners say must be produced.

c) By consumers, firms, and government choosing which goods and services to buy.

d) What will be produced is determined by what society needs the most.

27) In the country of Shem, the CPI is calculated using a market basket consisting of 5 apples, 4 loaves of bread, 3 robes and 2 gallons of gasoline. The per‐unit prices of these goods have been as follows: Using 2002 as the base year, what was the inflation rate between 2003 and 2004?

a) 28.5 percent

b) 34.2 percent

c) 47 percent

d) It is impossible to determine without knowing the base year.

28) Given the following information, calculate the unemployment rate: Full‐time employed = 80 Part‐time employed = 25 Unemployed = 15 Discouraged workers = 5 Members of underground economy = 6 Consumer Price Index = 110

a) 18.8 per cent.

b) 12.5 per cent.

c) 16.7 per cent.

d) 25 per cent.

29) If the quantity of resources available is fixed, as more of a good is produced, the opportunity cost of producing it increases. The most probable reason for this is that

a) as more of a good is produced, the quality of technology available to produce additional units declines.

b) the price of the inputs used to produce the good will rise.

c) consumers are unwilling to pay higher prices to cover the increases in production costs.

d) resources are not equally well‐suited to producing all goods.

30) Which of the following is a normative statement?

a) The current high price of petrol is the result of strong worldwide demand.

b) The price of petrol is too high.

c) Larger vehicles always use more fuel per kilometre than smaller vehicles

d) The supply of petrol has not been able to meet the demand for petrol.

31) Transfer payments are not included in GDP because

a) they do not generate income.

b) their market value is difficult to measure.

c) they are not purchases of goods or services.

d) their value is included in government expenditure.

32) The opportunity cost of going to your economics class

a) depends on the cost of your transport getting to class.

b) is equal to the highest value of alternative use of the time.

c) is zero because there is no admission charged if you are enrolled in the class.

d) depends on the salary of the lecturer.

33) Establishing employment agencies that speeds up the process of matching unemployed workers with unfilled jobs are an attempt to lower

a) cyclical unemployment.

b) seasonal unemployment.

c) structural unemployment.

d) frictional unemployment.

34) Suppose that money GDP for 2009 was $15 000 billion and the price index was 150 and in 2010 money GDP was $17 050 billion with a price index of 155. What is the rate of economic growth?

a) 5%

b) 10%

c) 2%

d) 1%

35) An individual has a comparative advantage in activity whenever she

a) also has an absolute advantage in that activity.

b) can perform the activity at a lower opportunity cost than another person can.

c) can do everything better than everyone else can.

d) can do the activity in less time than anyone else.

36) GDP is not a perfect measure of wellbeing because

a) GDP is adjusted for increases in drug addiction.

b) GDP is not adjusted for the effects of pollution.

c) GDP is adjusted for changes in crime.

d) the value of leisure is included in GDP.

37) What does an entrepreneur do in a market economy?

a) Organise the factors of production in a working unit.

b) Stand to lose the personal funds provided.

c) Develop the vision for the firm and ensure funding for the firm.

d) An entrepreneur does all of these things.

38) An example of a transfer payment is

a) the purchase of a new government office block.

b) a teacher's pay is transferred electronically from the government to the teacher.

c) interest repayments on a loan.

d) an unemployment benefit.

39) Which of the following is a microeconomics question?

a) What will be the level of total production in the national economy?

b) How much income will be saved and how much will be spent on consumer goods?

c) What factors determine the price of computers in the market?

d) Why is the rate of unemployment rising?

40) The measure of production that values production using current prices is called

a) value-added GDP.

b) nominal GDP.

c) black economy GDP.

d) real GDP.

41) Which of the following causes the official measure of the unemployment rate to understate the true extent of joblessness?

a) People who collect unemployment benefits report themselves to be searching for a job.

b) Discouraged workers are counted as unemployed.

c) Discouraged workers are not counted as unemployed.

d) Many full-time workers really want to be part-time workers.

42) A production possibility frontier will shift inwards if

a) inefficiency in production processes arise.

b) there is an increase in the rate of unemployment.

c) productive resources are destroyed due to war.

d) all of these options are correct.

43) Structural unemployment would increase when

a) discouraged workers drop out of the workforce.

b) the economy enters a recession.

c) the number of individuals who quit their job to find another increase.

d) workers are replaced by machines and the workers do not have the skills to perform new jobs.

44) The 2005 CPI was 196 and the 1982 CPI was 96.5. If your parents put aside $1,000 for you in 1982, how much would you have needed in 2005 in order to buy what you could have bought with the $1,000 in 1982?

a) $1,834.20

b) $2,031.09

c) $2,308.89

d) None of the above is correct.

45) What is an economic model?