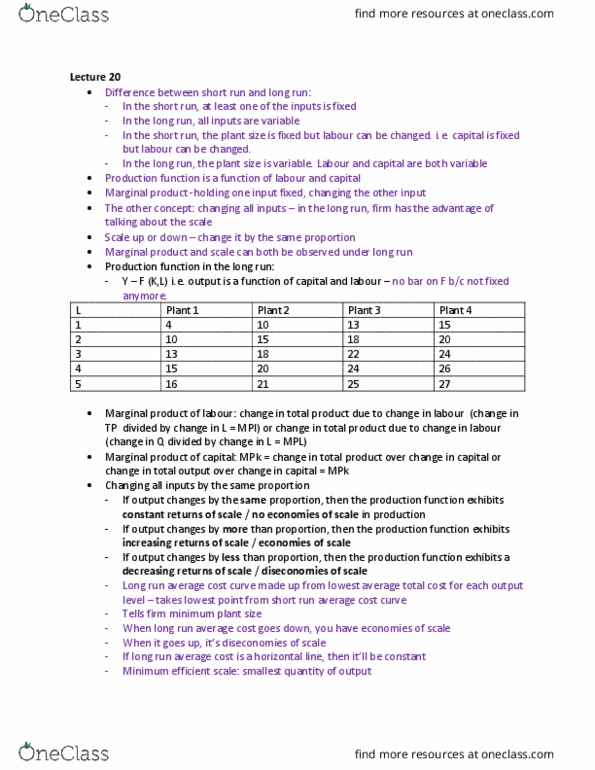

ECON101 Lecture 19: lecture 19

8 Nov 2018

School

Department

Course

Professor

ECON101 verified notes

19/25View all

Document Summary

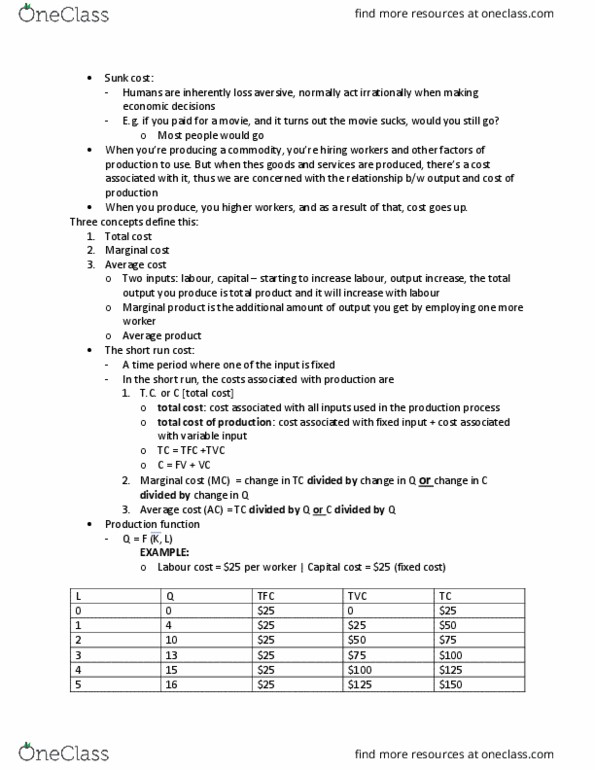

Humans are inherently loss aversive, normally act irrationally when making economic decisions. E. g. if you paid for a movie, and it turns out the movie sucks, would you still go: most people would go, whe(cid:374) (cid:455)ou"re produ(cid:272)i(cid:374)g a (cid:272)o(cid:373)(cid:373)odit(cid:455), (cid:455)ou"re hiri(cid:374)g (cid:449)orkers a(cid:374)d other fa(cid:272)tors of produ(cid:272)tio(cid:374) to use. A time period where one of the input is fixed. Example: labour cost = per worker | capital cost = (fixed cost) 5: diminishing returns: driving force of products and costs, long run cost: All inputs are variable: average cost (ac) Ac = tc divided by q or c divided by q. = tfc divided by q + tc divided by q. When marginal cost is down, it pulls the average cost low. Has to touch average cost at its lowest point (cid:894)i. e. (cid:373)ust tou(cid:272)h at (cid:448)erte(cid:454) as if it"s (cid:271)igger tha(cid:374), it pulls it uo(cid:895) When ac = mc, ac is at its minimum.