ECON206 Lecture 6: ECON 206 Lecture 6

29 Jan 2019

School

Department

Course

Professor

ECON206 verified notes

6/11View all

Document Summary

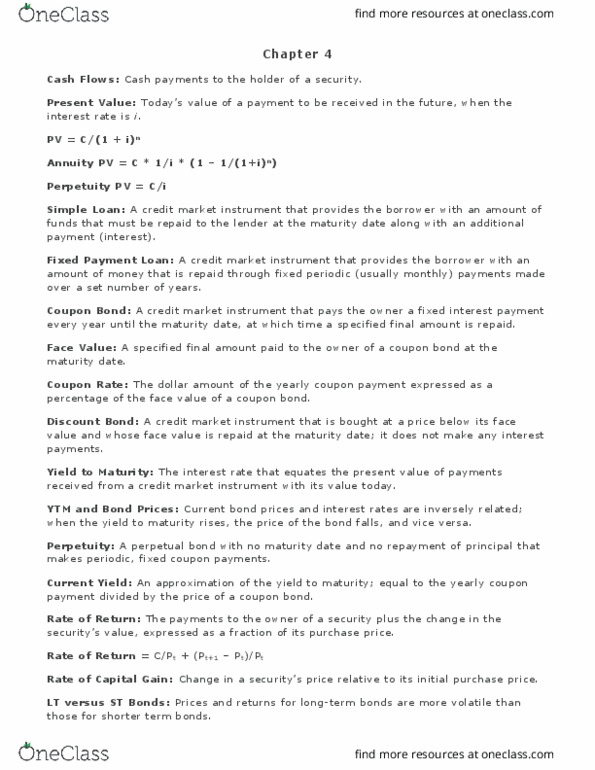

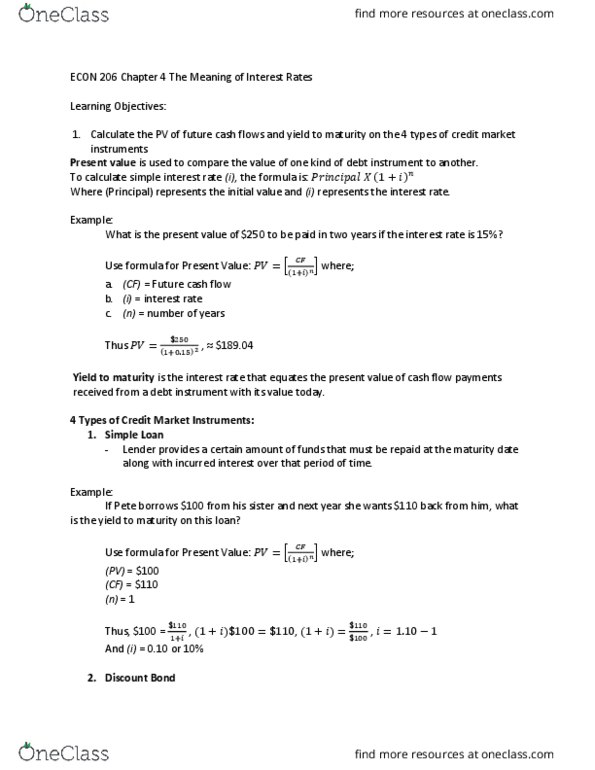

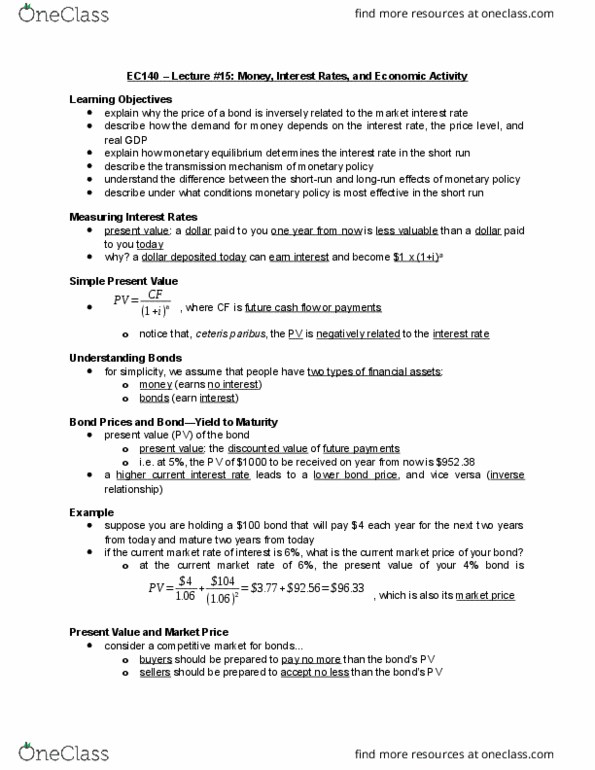

If price changes to i = (-)/ = 1. 1: changing interest rate calculation. Pv = cf/(1+i) cf: cash flow in one year. R = c/pt + (pt+1 pt)/pt: current yield: equation 5 p. 77, i=c/pt, yearly payment/price, rate of capital gain, change in bond"s price relative to initial purchase price, denoted g, ex. face value coupon bond purchased at par coupon rate. Interest rate risk: risk level associated with an asset"s return that results from interest-rate changes. Fisher equation: i = nominal interest rate, r = real interest rate, e = expected inflation rate i - r = e, ex ante real interest rate is adjusted for expected changes in the price level. The ender wants a real return of 8% and expects the inflation rate to be 2%. Therefore, the nominal interest rate is 10%: if, over the life of the contract, the inflation rate is 4%, the real return decreases to 6%, ex.