MTHEL131 Lecture Notes - With-Profits Policy, Demutualization, Mutual Organization

23 Nov 2013

School

Department

Course

Professor

Document Summary

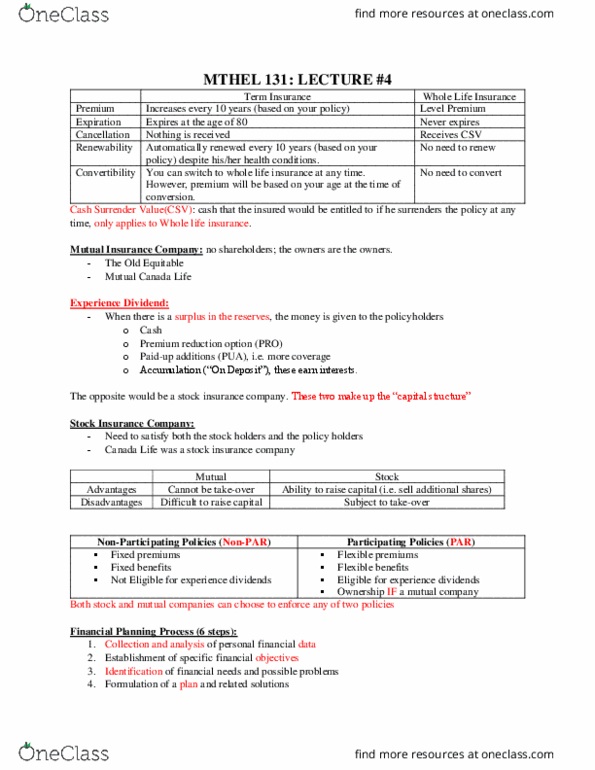

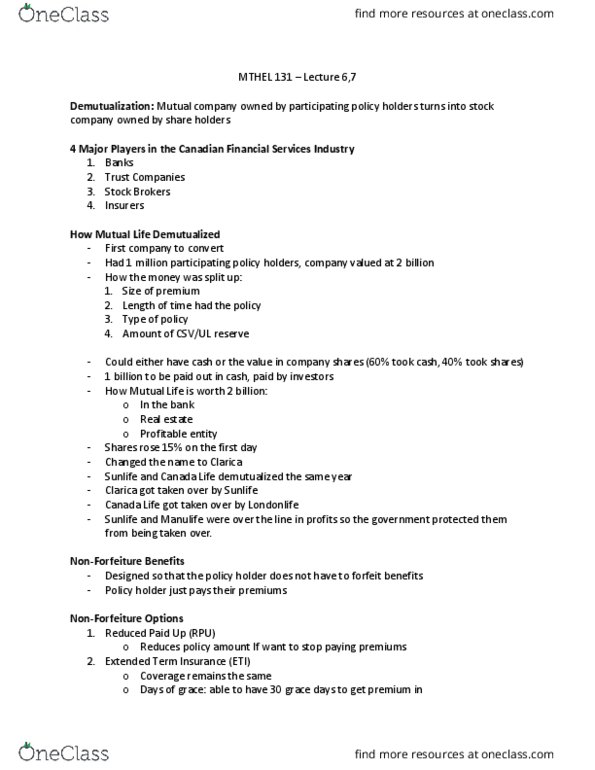

Participating policy holders are the owners of a mutual company. Mutual life led the way, and sooner, the 3 other largest mutual in canada, They went through the process, demutualize, that of being a mutual company owned by the shareholders, to stock owned by policyholders. At the transition point, participating policy holders" shares of the value in the company was unlocked. And the value is paid across participating policy holders in the form either cash or share. 2 primary reasons for diversification: the mutual company, now a stock have more ability to raise capital, the capital can allow them to grow and compete more effectively in the canadian finance services market place. It depends; general statement, say that most people would, over the long term, would like to become owner. When it comes to 2 types of insurances, the difference is do you want to rent or own.