MTHEL131 Lecture Notes - Lecture 6: Registered Retirement Savings Plan, Life Insurance, Common Rider

23 Nov 2013

School

Department

Course

Professor

Document Summary

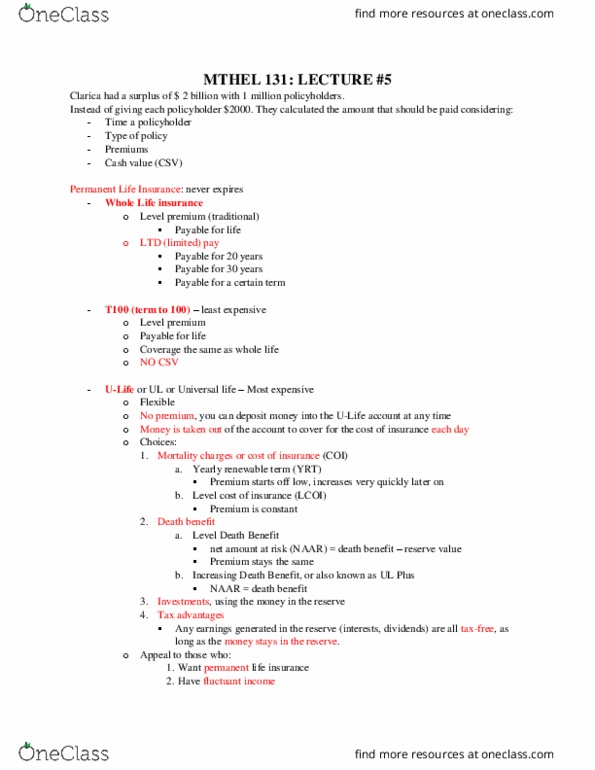

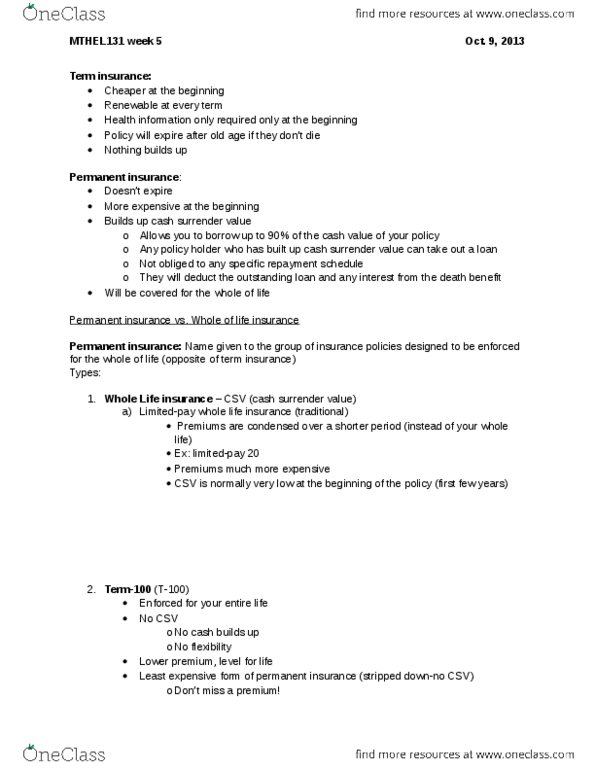

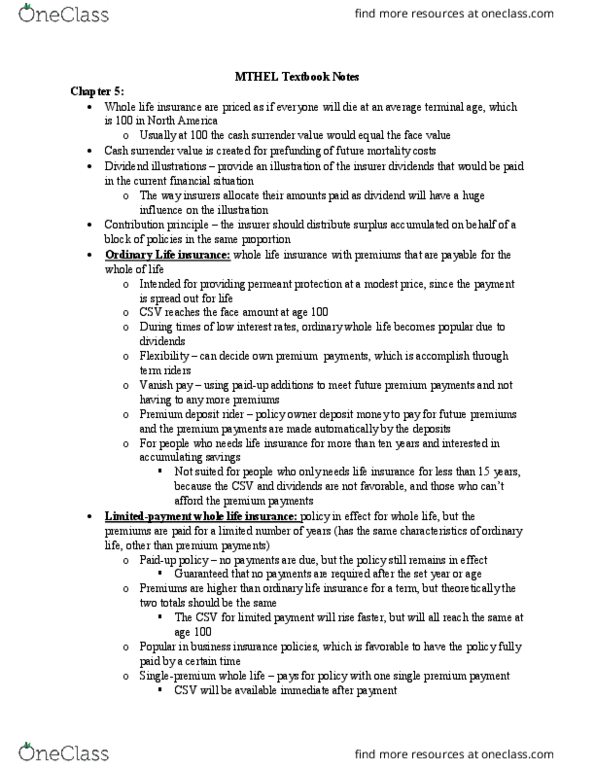

If you don"t pay the premium, no longer have the coverage: whole life (pay for whole life, limit pay whole life (common: limited pay 10 or 20 years, universal life (comparison to whole life): It has flexibility over how much you pay. Make deposit into your universal life account. As long as the insurer turn on the tap and take out the money, and money comes out, the policy stays enforce. If the deposit is dried up, or used up, the policy could lapse. With the universal life, if you have built up a sufficient amount in policy, you can take a certain period premium. If you have a traditional whole life policy, and now you need ,000 more, you need to buy another policy. If you have universal life, no need to buy a new policy, just let the keg last longer and tap open longer for every day (,000 ,000)