MTHEL131 Lecture Notes - Lecture 9: Disability Insurance, Worst-Case Scenario Series, Unemployment Benefits

23 Nov 2013

School

Department

Course

Professor

Document Summary

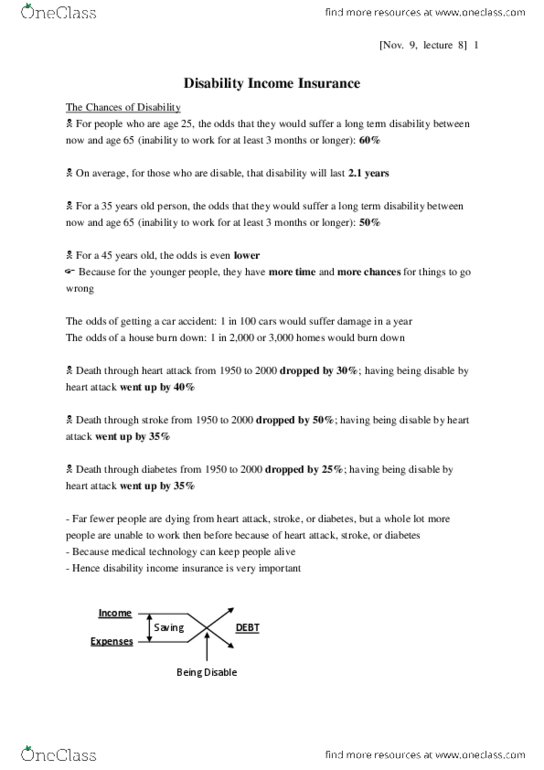

The underwriters believe that the moral hazard is higher the lower class; or the less the higher class. Pricing in disability income insurance is important role for actuary. Less expensive plans and policies are available to class 4 and 5, they are generally any occupation; and cannot go back work 3 days a week. But with the better policies for professions do have the flexibility to go back work 3 days a week. Tailoring the disability plan to their needs (3 processes): The insurer restrict the maximum amount to somewhere between 60%-70% gross income [ex. 67%] (they can purchase anything less than the maximum amount) A person earning ,000/month, can purchase maximum amount of disability benefit. Number of days that must pass from the day of the disability until you receive your first benefit payment. Generally waiting periods are expressed into 30, 60, 90, 180 days. [nov. 16, lecture 9] 2 less expensive the premium become.